MANM399 International Accounting and Finance Project Report Sample

Assignment Details

Report Structure

Your assignment guidelines may specify what should be included within the report.

Some suggestions on what a report could include:

• Title Page including name and date

• Table of contents indicates the structure of your report, showing the page number on which each section starts

• Executive Summary a detailed summary of your report. It provides the same purpose as an abstract in a research paper. Sometimes your audience will only read your executive summary so it needs to stand alone and fully represent your work within the report

• Main body must have Headings for example Background, Discussion, Conclusion, Recommendations

• References with all academic work, and beyond, you are expected to acknowledge the sources used within your report using the appropriate referencing system

• Appendices These should only be included when there is a requirement to enhance the information within the report.Referring to the appendix within your report is not meant

Visual communication

• Reports can include a range of visual sources:

• Tables

• Graphs (line, bar, histogram)

• Charts (bar, pie)

• Photographs

• Diagrams

• Info-graphics

• Maps and plans

• Interviews and observations

When using visual sources be mindful of copyright

Research/Evidence

Ensure the evidence and tables/graphs/statistics used within the report are appropriate and are linked to the point you are making. Visual resources are meant to enhance the meaning of your sections and can be used to present complex information in an accessible format.

• A 5,000 words report plus a 250 words executive summary

• A report based on very detailed research into company accounts

• Requires full mastery of all Excel techniques and formulae

• All this must be done INDEPENDENTLY

Solution

1. Company Introduction

Unilever Plc is a long-standing British multinational corporation specialising in consumer-packaged products, significantly influencing the global fast-moving consumer goods sector for more than a century (Unilever PLC, 2023). Unilever, a prominent entity in the business, was formed on September 2, 1929, due to the merger of Lever Brothers, a British soap manufacturer, and Margarine Unie, a Dutch margarine company. Over time, Unilever has grown to become a significant and influential presence in the market (GlobalData, 2023). The firm is based in London, England, and is dedicated to promoting sustainable living as a fundamental objective. This dedication serves as a guiding principle for the company's operations and is a key driver of its outstanding success (Unilever PLC, 2023).

Unilever's goods have a global reach, extending to over 190 countries and impacting the daily lives of more than 3.4 billion people. In 2022, the corporation had a noteworthy turnover of €60.1 billion, with a substantial 59% of that revenue originating from developing regions (Unilever PLC, 2023). The extensive worldwide presence of the company is facilitated by its wide-ranging assortment of more than 400 purpose-driven brands, some of which have attained sales above €1 billion. Significantly, it is worth mentioning that 14 of the company's brands have achieved a position inside the top 50 most selected fast-moving consumer goods (FMCG) brands globally (Unilever PLC, 2023). This serves as evidence of the company's lasting influence and significance. As an enterprise driven by a commitment to innovation, Unilever allocates a significant portion of its resources to Research & Development, directing a hefty sum of €908 million towards pioneering developments. The dedication to this endeavour has resulted in a gradual increase in revenue of €1.7 billion via the use of inventive solutions (GlobalData, 2023). Nevertheless, the company's commitment transcends just financial expansion and encompasses a steadfast adherence to environmental sustainability. With a total of 280 factories under its operation, the company has accomplished a noteworthy decrease of 68% in greenhouse gas emissions, showcasing its dedication towards fostering a more environmentally sustainable future (Unilever PLC, 2023).

The organisational structure is centred on five Business Groups, each with a distinct vision that is in harmony with its overall goal. "Beauty & Wellbeing" embodies a commitment to promoting inclusivity, fairness, and sustainability within beauty and wellbeing. The concept of "Personal Care" reflects its dedication to fostering beneficial transformations for individuals and the environment for university assignment help . The firm "Home Care" envisions a reimagined future for the cleaning industry, while its objective in "Nutrition" focuses on providing nutritious meals to 10 billion people while also prioritising environmental sustainability. Finally, "Ice Cream" revolves around generating pleasurable experiences within the several communities it caters to (Unilever PLC, 2023).

Unilever's dedication to being at the forefront of sustainability is evident via its recognition, including its constant top position as the leading corporate entity in the GlobeScan Sustainability Leaders Survey. The firm has maintained its place in the 'Masters' category of the Gartner Supply Chain Top 25 for five consecutive years, demonstrating its excellence in both financial and social responsibility criteria (Unilever PLC, 2023). In addition, Unilever was granted the esteemed Global Gold Glass by the S&P Corporate Sustainability Assessment in recognition of its extensive achievements in meeting environmental, social, and governance standards. This entity demonstrates exceptional performance when considering the domains of media, innovation, and efficacy (Unilever PLC, 2023). Unilever has achieved the highest ranking in the #Media100 for the fourth consecutive year, obtained second place in the #Creative100, and won the third position in the #Effective100 inside the prestigious WARC Rankings of 2023 (Unilever PLC, 2023).

1.1 Unilever Business Model

Unilever exhibits a strategy centred on purpose by effectively utilising its brands, people resources, and partnerships. This approach highlights a strong correlation between sustainability and exceptional performance. The company's function is beyond a conventional business since it catalyses constructive change, going beyond financial profits to create a sustainable societal influence (Figure 1).

.png)

Figure 1: Unilever Business Model

(Source: Unilever PLC, 2023)

Unilever demonstrates a steadfast dedication to achieving sustainable and equitable development by implementing the Unilever Sustainable Living Plan (USLP), which is prominent within the company's core values. This sustainable business model facilitates continuous development by mitigating risks, cultivating a competitive edge via creative ideas, decreasing expenses to improve profitability, and maintaining accountability, consequently bolstering confidence in the firm (Unilever PLC, 2023). The primary objectives of the USLP are to improve the health and well-being of more than 1 billion people by 2020, reduce the environmental footprint of goods by 50% by 2030, and simultaneously boost livelihoods and increase company operations by 2020. These aims have been effectively incorporated into the operational framework (Unilever PLC, 2023). The USLP, or Unilever Sustainable Living Plan, encompasses several strategies, such as conscientious procurement of agricultural raw materials, eco-conscious manufacturing practices, and purpose-driven brand marketing. It serves as a comprehensive framework to actualise Unilever's goal (Unilever PLC, 2023).

Unilever's success is founded upon the essential elements of innovation and teamwork. The corporation allocates €1 billion yearly to research and development activities, aiming to promote innovation by collaborating with academic institutions and suppliers (Unilever PLC, 2023). This strategic approach eventually leads to brand-driven advantages that align with emerging trends. Collaboration is crucial for Unilever as a central point connecting many stakeholders such as government entities, non-governmental organisations (NGOs), and a dynamic supply chain initiative known as "Partner to Win." This programme encourages suppliers to make creative contributions by providing incentives (Unilever PLC, 2023). The procurement teams of Unilever, who oversee €34 billion in purchases, are focused on enhancing profitability via increased efficiency and integrating the concepts of the Unilever Sustainable Living Plan (USLP) (Unilever PLC, 2023). It is worth mentioning that in 2016, a significant proportion of 51% of agricultural raw materials were procured from sustainable sources, therefore supporting well-established brands such as Knorr and Lipton. Moreover, consumer insight is pivotal in Unilever's business strategy, serving as the fundamental component that propels brand innovation (Unilever PLC, 2023). This is achieved through comprehending market dynamics by utilising various research methodologies. In addition, the broad geographical coverage of the organisation provides a degree of resilience against potential disturbances to local environments that may arise due to climate change (Unilever PLC, 2023).

1.2 Unilever Geographic Revenue

Unilever operates in three geographical areas which are Asia/AMET/RUB, The Americas and Europe. These geographic segments play a vital role for the company’s success and profitability. The following table and figure highlights Unilever’s revenue from the three distinct geographic locations.

.png)

Table 1: Unilever Regional Revenue

(Source: Unilever PLC, 2012; 2013; 2014; 2015; 2016)

The performance of Unilever as a whole and the dynamics of its many geographic regions are shown via an examination of sales data from 2012–2016 (Table 1). Sales in the Asia/Africa/Middle East/Russia/Turkey region (Asia/AMET/RUB) increased steadily from €20.4 billion in 2012 to €22.4 billion in 2016. This growth spells good news for the company's market position and customer demand. A consistent €17.1 billion in sales throughout the years from the Americas region demonstrates a secure market position and loyal customer base. Similarly, despite possible economic influences, Europe maintained stable revenues of roughly €13.2 billion (Figure 1). Unilever's revenue distribution exemplifies the company's global reach, focus on new markets, and ability to successfully navigate economic diversity, all of which position the company for stable growth and adaptability.

.png)

Figure 2: Unilever Regional Sales Chart

(Source:

2. Sectors Review

Unilever operates in four distinct business sectors; Personal Care, Foods, Home Care and Refreshments. The following tables highlight the sectoral revenue Unilever earned during 2012 to 2016.

2.1 Business Sector Revenue (2012-2016)

.png)

Table 2: Unilever Business Sector Sales % (2012-2016)

(Source: Unilever PLC, 2012; 2013; 2014; 2015; 2016)

After conducting an analysis of the sales distribution throughout the business sector of Unilever spanning 2012 to 2016, several significant observations may be inferred. Table 1 illustrates the proportion of overall revenues attributed to various company sectors over five years.

.png)

Figure 3: Unilever Business Sector Sales

(Source: Author)

2.1.1 Personal Care Sector

Unilever has consistently maintained a dominant position in the corporate environment, with its Personal Care division regularly accounting for the biggest proportion of overall revenues, ranging from 35% to 38%. The lasting relevance of Unilever is seen in its expertise in the personal care sector, which includes well-known brands associated with skincare, hygiene, and beauty items. The sector's strong growth is seen via consistent customer demand and significant financial benefits.

According to a report published by Statista.com (2023), it is projected that the cosmetics and personal care business will see development in all of its categories. Specifically, there is a forecasted increase in demand for sun protection and anti-ageing goods, indicating significant growth in these market segments. Emerging economies provide considerable opportunities since the increase in income levels allows customers to prioritise the efficacy of products and the quality of ingredients above less expensive alternatives. As a result, manufacturers prioritise the marketing of their products as better, transitioning their advertising strategies from price-based competition to emphasising product superiority.

The advent of the COVID-19 epidemic has expedited the digital transformation process, significantly changing the cosmetics and personal care industry towards a flourishing online landscape (Figure 4). The Beauty and Personal Care Products Market worldwide is predicted to grow substantially throughout the forecast period. It is estimated to be valued at USD 496.63 billion in 2023 and is expected to reach USD 622.45 billion by 2028, exhibiting a compound annual growth rate (CAGR) of 4.62% from 2023 to 2028 (Mordorintelligence, 2023). The post-COVID-19 period brought attention to dermatological concerns resulting from the heightened use of soap and sanitiser, resulting in a notable upswing in the market demand for personal care items. The cosmetics industry has also seen a market response to the increasing consumer desire for natural, non-toxic, and organic ingredients. The increasing worldwide use of organic personal care products may be attributed to customer demand for natural ingredients (Mordorintelligence, 2023).

.png)

Figure 4: Personal Care Market Growth

(Source: Mordorintelligence.com, 2023)

Unilever's sustained achievements in the Personal Care sector are congruent with the positive growth trend in the global cosmetics and personal care market. Unilever has a strategic edge in capitalising on future development potential due to the sector's resiliency during the pandemic and the increasing customer awareness about natural and organic goods.

2.1.2 Food Sector

The Food business of Unilever demonstrated a continuous and stable contribution to the company's total revenues, maintaining a range of 24% to 28% during the monitored period (Statista, 2023b). Although there was a little decline in the sector's proportion, it maintained a substantial portion of the company's overall revenues. Notably, despite a little decrease, Unilever's food items continued to have a robust market position (Statista, 2023).

According to the data provided by Statista.com (2023b), the global food market is anticipated to see sustained expansion, with a predicted surge of 3.6 trillion U.S. dollars (+38.46%) from 2023 to 2028. The current year signifies a decade-long trend of increasing revenues, projecting a high value of 12.96 trillion U.S. dollars in 2028 (Figure 5). One section of the industry that stands out is Confectionery & Snacks, projected to have a market volume of US$1.7 trillion by 2023 (Mordorintelligence, 2023b). When examining geographical comparisons, it becomes evident that China is projected to be the leading revenue producer, with an estimated revenue of US$1,492 billion by 2023. The observed expansion is consistent with a per capita revenue of US$1,218.00 for the same period, indicating the strong worldwide success of the industry (Mordorintelligence, 2023b). According to projections, the anticipated volume of the Food market is expected to reach 3,117.0 billion kilograms by 2028, signifying a growth rate of 4.3% in volume by 2024 (Statista, 2023b). Additional analysis indicates that the projected average volume per individual within the Food market will reach 340.70 kilograms by 2023 (Statista, 2023b). Hence, as Unilever strategically manoeuvres within the sector, it can leverage the industry's upward trajectory and effectively respond to changing consumer preferences and emerging trends.

.png)

Figure 5: Food Industry Revenue Growth

(Source: Statista.com, 2023b)

2.1.3 Refreshment Sector

The Refreshment sector, which accounted for around 19% of total sales between 2012 and 2016, has consistently performed within Unilever's business activities. The refreshment sector of Unilever comprises various items such as ice cream, tea, and drinks. This indicates that Unilever has successfully maintained a stable client base for its refreshment services.

As of 2023, the Refreshment or Snack Food market had generated worldwide revenue of US$539.3 billion. According to projections, there is an expected compound annual growth rate (CAGR) of 6.34% between 2023 and 2028 (Figure 6) (Mordorintelligence, 2023b). Significantly, the United States appears as a prominent source of income, generating a substantial amount of US$110 billion in 2023. The per capita revenues for the same year total US$70.21. According to projections, the anticipated volume of the Refreshment market is predicted to reach 81.0 billion kilograms by 2028, exhibiting a projected growth rate of 4.4% in 2024 (Statista, 2023c). The mean volume per individual within this market is projected to reach 8.8 kilogrammes by the year 2023.

.png)

Figure 6: Global Refreshment or Snack Food Industry Growth

(Source: Mordorintelligence, 2023b)

In recent times, there has been a notable change in consumer inclinations towards meal alternatives that are quick and readily available, resulting in a significant increase in the market demand for snack foods. Manufacturers have reacted to the need for convenient nutrition options by creating goods fortified with protein, vitamins, and other nutrients. These products are specifically designed to meet the dietary requirements of those with busy lifestyles (Statista, 2023c). Mondelez International's 2021 research indicates that 72% of individuals actively seek portion-controlled alternatives. The consumption of refreshment food has increased due to its alignment with evolving consumer patterns. The motivating reasons are convenience, premiumisation, innovation, and nutritional value (Mordorintelligence, 2023b). The COVID-19 epidemic has allowed private snack food companies to meet the heightened demand. Refreshment food consumption is very prevalent in the Asia-Pacific region, which has the biggest market share. This may be attributed to urbanisation and the proliferation of Western dietary practices (Mordorintelligence, 2023b). Developing nations such as India and China have a substantial role in fostering this expansion. Unilever Plc has established itself as a prominent player in the Refreshment Food industry. Therefore, the steady contribution of Unilever's Refreshment business aligns with the prevailing worldwide trend of heightened snack food consumption. Unilever's dominant market position enables them to use the changing needs within the snack food business strategically (Mordorintelligence, 2023b).

2.1.4 Home Care Sector

.png)

Figure 7: Home Care Industry Growth

(Source: Mordorintelligence, 2023a)

The sales contribution of the Home Care industry had a stable pattern, with fluctuations between 18% and 19% over the indicated time frame. Although the smallest of the four industries, it significantly influenced Unilever's total revenue (Mordorintelligence, 2023a).

According to the research, the home care industry is projected to undergo a Compound Annual Growth Rate (CAGR) of 4.67% throughout the specified period. Following the COVID-19 pandemic, there has been a notable rise in consumer awareness about personal and household cleanliness (Mordorintelligence, 2023a). It is worth noting that there has been a substantial increase in online consumer expenditure, which has greatly contributed to the growth of online sales in the home care sector. Prominent industry leaders, including Procter & Gamble, Henkel AG, Unilever, Church & Dwight, and the Reckitt Benckiser Group, are leading in the market, providing home care solutions worldwide. As customers are increasingly more knowledgeable and aware of environmental issues, prominent industry participants embrace sustainable practices (Mordorintelligence, 2023a). In June 2021, Unilever PLC unveiled a pioneering paper-based laundry detergent container that does not have supplementary layers of plastic. Implementing these novel advancements is driving the home care industry towards achieving environmental sustainability and promoting the creation of cleaner living environments (Mordorintelligence, 2023a). Hence there is a need to advance cleaning and domestic maintenance items constantly. The need to remain competitive necessitates the development of inventive, economically viable, potent, and proficient solutions.

Major Home Care Market Trends:

? Increasing Focus on Home Hygiene: The significance of hygiene practices has been heightened by the COVID-19 epidemic, extending beyond basic cleanliness. The COVID-19 pandemic has precipitated a significant change in consumer behaviour, characterised by heightened awareness and emphasis on cleanliness practices. Nations such as India, characterised by increasing families, rising disposable income, and enhanced buying power, saw a notable upswing in demand for home care and hygiene goods (Mordorintelligence, 2023a).

? International Impact: In the wake of the COVID-19 pandemic, home care goods have been used in countries such as China, Japan, and Australia. Prominent companies in the industry, including P&G, Unilever, and The Clorox Company, are strategically adapting their product portfolios to meet the evolving demands of consumers, therefore stimulating an increase in revenue (Mordorintelligence, 2023a).

3. Company Assessment

To determine Unilever’s historic financial performance and its future growth prospect, 5 FY financial ratios are analysed. The following section analyses Unilever’s performance, liquidity, solvency and efficiency with the help of several financial ratios. The section also compares Unilever’s performance with its competitors.

3.1 Industry Competitors

Unilever, a well-established consumer packaged goods corporation, operates within a highly competitive market with industry leaders such as Johnson & Johnson, Nestle, Procter & Gamble, and Reckitt Benckiser Group. Each of these businesses has a significant worldwide reach and various brands across several industries. Johnson & Johnson is well recognised for its extensive range of healthcare and pharmaceutical products, whereas Nestle has a prominent position as a leading entity within the food and beverage industry. Procter & Gamble is well known for its extensive range of household and personal care goods, whereas Reckitt Benckiser Group focuses primarily on producing and distributing health, hygiene, and home products. These organisations engage in a battle for market share and customer loyalty by using strategies like innovation, strategic acquisitions, and sustainability programmes. This leads to intense competition within the fast-moving consumer goods sector.

3.2 Growth Rate

In Table 3, we can see that Unilever and its rivals, Johnson & Johnson, Nestle, Procter & Gamble, and Reckitt Benckiser Group, all saw different revenue growth rates from 2012 to 2016.

.png)

Table 3: Unilever and its competitors revenue growth rate

(Source: Annual Report (2012-2017) Unilever; Johnson & Johnson; Nestle; Procter & Gamble; Reckitt Benckiser Group)

Table 3 shows how the organisations' performance trajectories have drastically shifted over time. Unilever's growth rate has been erratic, with a sharp 10% gain in 2012 followed by 3% declines in both 2013 and 2014. It's important to remember that after a significant growth of 10% in 2015, there was a little reduction of 1% in the following year, 2016. Changes in consumer preferences, new product releases, intense competition, and shifting economic conditions are all possible explanations for the fluctuations. Johnson & Johnson's development followed a mixed pattern of good and bad, with a 5% decline in 2012 followed by 6% and 4% increases in 2013 and 2014, respectively. After dropping by 6% in 2015, 2016 saw a modest uptick of 3%. Alterations in healthcare demand, legislative shifts, and tactical actions all contributed to this improvement.

In addition, between 2013 and 2016, Nestle's growth rates were close to 0%, with very minor swings. Performance at Procter & Gamble has steadily declined, falling by 8% in 2015 and 15% in 2016. Increased competition, shifting consumer preferences, and other challenges might all be to blame for the decline. There were fluctuations in Reckitt Benckiser Group's financial performance, the largest of which being a 12% decline in 2014. Several factors, including the nature of the market and the popularity of its goods, have contributed to these shifts. Figure 8 depicts the complex interplay between customer habits, competition, economic conditions, and strategic choices and how they all influence revenue paths.

.png)

Figure 8: Unilever and Competitor Revenue

.png)

Table 4: Unilever growth rate

(Source: Annual Report (2012-2017) Unilever; Johnson & Johnson; Nestle; Procter & Gamble; Reckitt Benckiser Group)

The revenue growth of Unilever exhibited variability across the specified time frame, commencing with a positive growth rate of 10% in 2012, followed by consecutive falls of -3% in 2013 and 2014. In 2015, there was a significant increase of 10%, followed by a little decrease of -1% in 2016. The observed oscillations may be attributed to factors such as market dynamics, customer preferences, and prevailing economic situations. Positive growth may be ascribed to the successful introduction of new products and expansion into new markets. On the other hand, reductions in growth might be attributable to heightened competition or shifts in consumer spending patterns.

Furthermore, Unilever has regularly shown a favourable operating profit and net income trend. The corporation demonstrated its adeptness in cost management and operational efficiency by the yearly growth rates of its operating profit, which were 9%, 8%, 6%, -6%, and 4%. Likewise, a favourable trend was seen in the rise of net income, with rates of 7%, 6%, 5%, -5%, and 5%. These patterns highlight Unilever's ability to manage costs and sustain profitability effectively.

.png)

Figure 9: Unilever growth rate

(Source: Author)

3.3 Performance

The financial performance trends of these companies throughout time are broken down in Tables 5-9. Market dynamics, customer preferences, regulatory changes, and economic conditions are only a few of the external factors that impacted the observed trends. Internal issues including operational efficiency, cost management, and innovation strategies are also cited as causes of the discrepancies.

The ability to convert sales into profits is measured by the Net Income Margin indicator. Reckitt Benckiser Group, Unilever, and Johnson & Johnson all kept their margins stable and showed consistent profitability throughout time. Changes in operational conditions, competitive pressure, and the use of cost-cutting measures are only some of the possible explanations for the ups and downs in profit margins seen by Nestle and Procter & Gamble. Asset Turnover is used as a measure of asset utilisation efficiency. Unilever's consistently high asset turnover rates are indicative of the company's ability to convert its resources into profit. Nestle and Procter & Gamble, on the other hand, have lower asset turnover percentages, indicating the existence of larger asset bases that need more substantial revenue generating.

Return on equity (ROE) measures how well a firm generates profits for its shareholders. Profitability was driven by asset turnover and financial leverage at both Johnson & Johnson and Reckitt Benckiser Group. The return on equity (ROE) for Unilever and Nestle was consistent throughout time. However, Procter & Gamble's ROE fluctuated, which may have been caused by shifts in operating conditions and the company's financial structure. According to the profitability ratios, Johnson & Johnson has consistently achieved high levels of profitability across a variety of metrics, with good profit margins and efficient operational practises being the primary drivers of this success. Reckitt Benckiser Group's high margins and profits may be traced back to the company's strategic use of efficient business practises. Profitability ratios were more inconsistent at Procter & Gamble than they were at Unilever and Nestle.

.png)

.png)

Table 5: Unilever Dupont and Profitability Analysis

(Source: Annual Report (2012-2017) Unilever)

Profitability

.png)

.png)

Table 6: Johnson & Johnson DuPont and Profitability Analysis

(Source:Annual Report (2012-2017) Johnson & Johnson)

.png)

Table 7: Nestle DuPont and Profitability Analysis

(Source:Annual Report (2012-2017) Johnson & Johnson)

Profitability

.png)

Table 8: Procter & Gamble DuPont and Profitability Analysis

(Source: Annual Report (2012-2017) Procter & Gamble)

Profitability

.png)

.png)

Table 9: Procter & Gamble DuPont and Profitability Analysis

(Source: Annual Report (2012-2017) Reckitt Benckiser Group)

3.4 Liquidity and Solvency

A company's ability to meet its short-term financial obligations may be gauged using liquidity metrics like the Current Ratio, Quick Ratio, and Cash Ratio. Table 10-14 shows that between 2012 and 2014, Unilever had a decline in its liquidity ratios. Multiple causes, including the evolution of markets, the company's expansion initiatives, and careful stock management, have contributed to this decline. Due to its diversified income streams and efficient working capital management, Johnson & Johnson has continuously maintained solid liquidity ratios throughout the years. Demand changes in the market for Nestle's consumer goods led to a mixed bag of results for the company. Procter & Gamble has a healthy liquidity position thanks to its market dominance and well-managed supply chain, as shown by the company's liquidity ratios. Reckitt Benckiser Group's liquidity ratios have steadily increased, which is indicative of the company's improved management of working capital.

Solvency measures, such as the Debt to Equity Ratio and Interest Coverage Ratio, are used to assess the enduring financial stability of a corporation. Unilever, Johnson & Johnson, Nestle, and Procter & Gamble had consistent debt-to-equity ratios, indicating proficient debt management tactics. The Reckitt Benckiser Group had a downward trajectory, indicative of endeavours to alleviate its financial obligations. The interest coverage ratios for all firms typically stayed at levels that provide sufficient coverage for interest payments.

External causes, including economic cycles, interest rate changes, and business rivalry, impacted these developments. Internal elements that contribute to these results include effective working capital management, smart debt allocation, and wise financial choices. One example is the case of Johnson & Johnson, where the company's robust liquidity and minimal debt ratios can be attributed to its broad healthcare portfolio. On the other hand, Nestle's varying liquidity ratios can be associated with fluctuations in consumer behaviour.

.png)

Table 10: Unilever Liquidity and Solvency Analysis

(Source: Annual Report (2012-2017) Unilever)

.png)

Table 11: Johnson & Johnson Liquidity and Solvency Analysis

(Source: Annual Report (2012-2017) Johnson & Johnson)

.png)

Table 12: Nestle Liquidity and Solvency Analysis

(Source: Annual Report (2012-2017) Nestle)

.png)

Table 13: Procter & Gamble Liquidity and Solvency Analysis

(Source: Annual Report (2012-2017) Procter & Gamble)

.png)

Table 14: Reckitt Benckiser Liquidity and Solvency Analysis

(Source: Annual Report (2012-2017) Reckitt Benckiser Group)

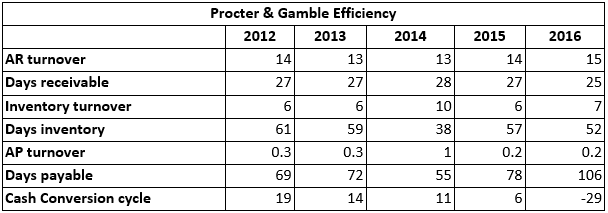

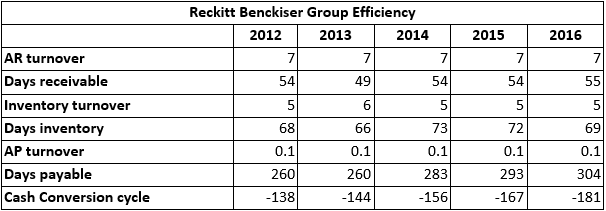

3.5 Efficiency

Table 15 shows that Unilever consistently maintained a relatively high Accounts Receivable (AR) turnover, indicating its ability to efficiently collect payments from customers. The company's Days Receivable figures remained steady, suggesting effective credit management. Similarly, Unilever's Inventory turnover ratios remained consistent, indicating efficient inventory management practices. The company's Accounts Payable (AP) turnover and Days Payable figures also remained stable, reflecting balanced supplier relationships and payment practices. As a result, Unilever managed to consistently maintain a negative Cash Conversion Cycle (CCC), showcasing its capability to effectively manage its working capital and convert investments into cash flows.

Comparatively, while Unilever's competitors like Johnson & Johnson, Nestle, Procter & Gamble, and Reckitt Benckiser Group demonstrated varying degrees of efficiency,

Unilever's stable and competitive efficiency ratios highlight its effective operational strategies (Table 15-19). The trends attributes to Unilever's focus on supply chain optimization, effective credit management, and responsive inventory control practices. Moreover, external factors like market conditions, industry trends, and competitive pressures also played an important role. However, Unilever's consistent performance across these efficiency metrics stems from its emphasis on lean operations, technology-driven supply chain management, and customer relationship management strategies.

In conclusion, Unilever's efficiency ratios demonstrate its strong operational performance relative to its competitors. The company's efficient working capital management and balanced approach to AR, inventory, and AP management have likely contributed to its competitive edge in this aspect.

.png)

Table 15: Unilever Efficiency Analysis

(Source: Annual Report (2012-2017) Unilever)

.png)

Table 16: Johnson & Johnson Efficiency Analysis

(Source: Annual Report (2012-2017) Johnson & Johnson)

Table 17: Nestle Efficiency Analysis

(Source: Annual Report (2012-2017) Nestle)

.png)

Table 18: Procter & Gamble Efficiency Analysis

(Source: Annual Report (2012-2017) Procter & Gamble)

Table 19: Reckitt Benckiser Group Efficiency Analysis

(Source: Annual Report (2012-2017) Reckitt Benckiser Group)

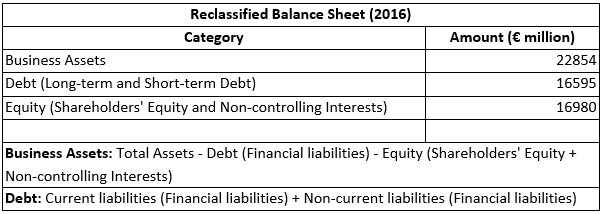

4. Reclassification of Financial Statements

Table 20: Unilever Reclassified Income Statement (2016)

(Source: Annual Report 2016 Unilever)

Table 21: Unilever Reclassified Balance Sheet (2016)

(Source: Annual Report 2016 Unilever)

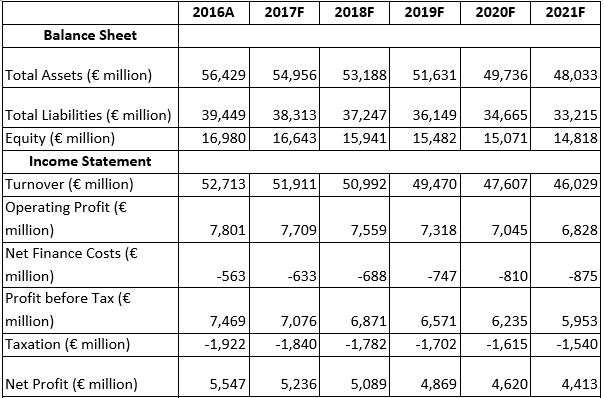

5. Financial Statements Forecasting

The findings from the previous section has been used to determine the forecasted values for Unilever (2017-2021). A unified forecasted financial statement for the year 2017-2021 is provided. It is followed by an explanation on the key drivers of the forecasted figures.

Table 22: Forecasted Balance Sheet & Income Statement (2017-2021)

(Source: Author)

A junction of causes mostly drives the anticipated decline in overall assets. Significantly, the decrease in turnover assumes a crucial function, suggesting that the organisation may have difficulties generating increased revenue. This observation is substantiated by the decline in the asset turnover ratio, indicating a deterioration in the company's ability to utilise its assets for revenue generation effectively. Therefore, these factors play a role in reducing the entire asset base. The decrease in total liabilities on the liabilities side can be ascribed to a reduction in current obligations. This phenomenon can be mostly attributed to reduced trade payables and other current obligations. The observed decrease in this metric may indicate an enhanced capacity to effectively handle immediate financial responsibilities, highlighting the company's efforts to strengthen its financial adaptability. The decline in equity, a notable constituent of the balance sheet, can be attributed to the reduced net profit. The phenomenon is contingent upon combining many factors influencing employee attrition, operational earnings, and financial expenses.

The anticipated decrease in employee turnover is a result of various complex factors. A reduction in asset turnover, which indicates the company's effectiveness in earning revenue from its assets, directly contributes to the drop in turnover. Furthermore, the decline in net income margin, a crucial metric for assessing profitability, also contributes to the reduction in overall revenue figures. The decrease in operational profit might be attributed to a combination of various factors. Significantly, the reduction in turnover directly impacts the company's financial performance.

Moreover, a declining operating margin, influenced by factors impacting gross profit and operating expenses, negatively impacts the operating profit metric. The upward trend in net finance costs can be attributed to a rise in expenses related to financing, accompanied by a decrease in income generated from financing activities. The components of finance are influenced by fluctuations in interest rates, variations in debt levels, and changes in investments. The decline in pre-tax profit results from multiple factors, including changes in revenue, operating profit, and net finance expenses. This also includes the impacts of peripheral items and other income or loss arising from investments held for the long term. The decrease in net profit can be attributed to the diminished pre-tax earnings and the subsequent influence of taxes. Consequently, this impacts both shareholders' equity and non-controlling parties' interests.

The tendencies in projected data collectively indicate probable challenges in generating revenue, controlling costs, and efficiently managing financial obligations. The issues are further emphasised by the decline in key performance indicators, such as net income margin, asset turnover, and return on assets. The observed decline in equity and profitability ratios, such as return on equity, indicates a potential strain on the overall value of shareholders.

Based on the projected financial statements the following Free Cash Flow to Equity (FCFE) is calculated.

Table 23: Forecasted Balance Sheet & Income Statement (2017-2021)

(Source: Author)

6. Cost of Capital (CAPM to calculate cost of equity)

The Capital Asset Pricing Model (CAPM) is a prevalent approach utilised in estimating the anticipated equity return for a company, considering its risk profile and the broader market environment (Pramono et al. 2022). The risk-free rate refers to the hypothetical rate of return that an investor can get without assuming any level of risk (Fernandez et al. 2020). The risk-free rate of Unilever is 4.44%.

Beta is a metric that quantifies the degree of responsiveness of a stock's returns to fluctuations in the broader market's returns. A beta value of 1 signifies that the stock correlates with the market, implying that its price movements align with the overall market. Conversely, a beta value below 1 suggests that the stock has lower levels of volatility in comparison to the market (Huy and Hang, 2021). Unilever exhibits a beta coefficient of 0.17, suggesting a lower volatility level than the broader market (Yahoo!Finance, 2023). Furthermore, the market return refers to a market index's retrospective mean yearly return, such as the FTSE 100. Historically, The average market return from 2017 to 2021 has been recorded at 3.36% (Yahoo!Finance, 2023).

Table 23 shows the cost of equity (Re) determined by the Capital Asset Pricing Model (CAPM) is 4.25%. This figure signifies the anticipated return that investors would demand to participate in the company, considering its level of risk and the prevailing market conditions.

Table 24: Cost of Equity

(Source: Author)

7. Valuation

7.1 Constant Growth Dividend Discount Model (Gordon Growth Model)

The Constant Growth Dividend Discount Model (DDM) is a valuation method that determines the worth of a stock by projecting future dividend payments and discounted them to their current value (d'Amico and De Blasis, 2020). In the instance of Unilever, given a dividend growth rate (g) of 4% and a needed rate of return (r) of 11.30%, the Dividend Discount Model (DDM) calculation results in a stock value of €42.31, as presented in Table 25.

Additionally, the Dividend Discount Model (DDM) is characterised by its simplicity in application and interpretation, rendering it easily accessible to both investors and analysts. The Dividend Discount Model (DDM) emphasises the potential return derived from dividend income, making it an attractive option for investors prioritising income generation (Xu, 2022). This is particularly relevant for companies with a track record of consistently paying dividends. Moreover, it is highly effective for corporations that exhibit consistent financial success and possess predictable rates of dividend increase (d'Amico and De Blasis, 2020).

Nevertheless, it should be noted that the Dividend Discount Model (DDM) operates under the assumption of a consistent growth rate that continues indefinitely. This assumption may not accurately reflect the reality for companies operating in changing market environments (Xu, 2022). The scope of the model's application is restricted to corporations that exhibit a continuous pattern of dividend payments while excluding those who choose to reinvest their earnings to achieve growth. Minor adjustments in the pace of growth or the expected return can result in substantial variations in the valuation result (Xu, 2022).

Table 25: Valuation using DDM

(Source: Author)

7.2 Discounted Cash Flow (DCF) Method

The discounted cash flow (DCF) approach evaluates a company's valuation by considering the current value of anticipated future cash flows (Laitinen, 2019). The process entails making predictions about the Free Cash Flow to Equity (FCFE) for a specified forecast duration, followed by the computation of the terminal value beyond such duration (Sutjipto et al. 2020). The valuation of Unilever is determined through the utilisation of Free Cash Flow to Equity (FCFE) predictions, combined with a terminal value of €1,806.80. This approach results in a discounted cash flow (DCF) valuation of €19,134.50, as presented in Table 26. This methodology facilitates the incorporation of fluctuating growth rates, hence providing increased adaptability in capturing the dynamic prospects of an organisation (Laitinen, 2019).

The discounted cash flow (DCF) methodology encompasses the complete range of cash flows, offering a comprehensive perspective on a company's intrinsic worth. In contrast to the Dividend Discount Model (DDM), the Discounted Cash Flow (DCF) approach can accommodate fluctuating growth rates and periods, rendering it flexible and suitable for enterprises operating within dynamic market environments (Sutjipto et al. 2020). The Discounted Cash Flow (DCF) method acknowledges the principle that the present value of a euro surpasses its future value, as it incorporates the concept of the time value of money in the valuation process (Sutjipto et al. 2020).

Nevertheless, the discounted cash flow (DCF) method entails predicting numerous factors, introducing uncertainty and intricacy into the valuation process. The precision of the valuation is significantly influenced by the precision of input assumptions, which might provide difficulties in forecasting, particularly for long-term forecasts. The determination of the terminal value necessitates the consideration of assumptions about perpetuity growth rates and discount rates, both of which possess the potential to exert a substantial influence on the ultimate valuation outcome (Laitinen, 2019).

Table 26: Valuation using DCF

(Source: Author)

8. Sensitivity Analysis

.png)

Table 27: Sensitivity Analysis

(Source: Author)

Constant Growth Dividend Discount Model (DDM) noted that an increase in the growth rate (g) leads to a corresponding increase in the projected value of the stock. The observed correlation is consistent with the inherent characteristics of the model, wherein a greater growth rate signifies a more rapid increase in dividends, resulting in a higher assessment of value. Nevertheless, it is crucial to acknowledge that the DDM model operates under the assumption of a perpetual and consistent growth rate, which may not always accurately represent actual circumstances in the real world (Xu, 2022). The sensitivity analysis underscores the significance of selecting a reasonable and well-founded growth rate, as it is crucial for maintaining the precision of the valuation (Table 27).

Conversely, the discounted cash flow (DCF) value is susceptible to variations in the cost of equity (r). As the cost of equity rises, there is a corresponding fall in the assessed valuation of the company. The observed result aligns with the underlying principle of the discounted cash flow (DCF) model, which posits that an elevated cost of equity corresponds to an increased discount rate (Laitinen, 2019). Consequently, this leads to a diminished present value of forthcoming cash flows. The sensitivity analysis emphasises the need for precise estimation of the cost of equity, which entails the evaluation of the company's risk profile and market conditions (Sutjipto et al. 2020).

Both valuation approaches possess distinct advantages and downsides. The Constant Growth Dividend Discount Model (DDM) offers a straightforward and comprehensible approach to valuing stocks. However, its applicability may be limited for certain companies, particularly those that exhibit erratic dividend payments, due to its dependence on perpetual growth assumptions and payouts. Although possessing greater comprehensiveness and flexibility, the discounted cash flow (DCF) method necessitates a meticulous assessment of input variables and might exhibit sensitivity to alterations in assumptions. Additionally, it considers the complete cash flow profile, enhancing flexibility in response to evolving business circumstances. In summary, the sensitivity analysis reveals that minor fluctuations in growth rates and cost of equity can result in substantial fluctuations in the estimated valuation of Unilever.

9. Price Multiples

Table 28: Price Multiples

(Source: Author)

Table 28 provides significant information regarding the market's perception of Unilever's financial performance and growth prospects. Price multiples, often called valuation ratios, concisely represent the extent to which investors are ready to allocate funds towards a company's earnings, book value, or sales. The P/E ratios of Unilever demonstrate a moderate valuation, implying that investors are inclined to pay a justifiable price concerning the company's present and anticipated future earnings. The forward price-to-earnings ratio (P/E) of 17.74 suggests that there are elevated expectations for future earnings growth (MarketWatch, 2023). Furthermore, the elevated price-to-book (P/B) ratio of Unilever may be ascribed to its robust assortment of brands, expansive international presence, and promising avenues for expansion. Finally, it can be observed that Unilever's price-to-sales (P/S) ratio of 2.02 signifies that investors are prepared to pay a justifiable multiple of the company's sales considering its potential for growth and well-established position in the market (Ycharts, 2023).

The price multiples offered collectively indicate that Unilever is perceived as a reputable and well-established corporation with favourable prospects for growth. The valuation metrics, specifically the forward price-to-earnings (P/E) ratios, suggest that investors hold a positive outlook for the company's anticipated growth. Unilever's strong market position and consistent earnings history within the consumer goods industry may have contributed to the positive feeling. Investors place a high value on Unilever's brand equity and worldwide market presence, which are reflected in the company's high P/B ratio. This finding indicates that investors think the firm will be able to put its assets to good use in order to grow and become more profitable in the future. The market is willing to pay a reasonable premium for Unilever's sales because of the company's dominant position in its industry and its proven ability to make profits, as shown by the stock's price relative to its sales (P/S) ratio.

10. Recommendation and Conclusion

Drawing upon a thorough examination of Unilever's financial analysis and valuation techniques, meaningful insights are derived and offer suggestions for prospective investors. Based on the analysis of forecasts and ratios, it can be inferred that Unilever demonstrates a consistent and steady financial performance. The projected income statements demonstrate a steady increase in revenue and net profit throughout the years, accompanied by robust net income margins and return on equity ratios, which signify effective profitability and efficient utilisation of assets. The balance sheet reveals a favourable equity multiplier and a satisfactory debt-to-equity ratio, illustrating a well-balanced capital structure.

The cost of equity, as determined through applying the Capital Asset Pricing Model (CAPM), demonstrates a strong correlation with the market return. This correlation indicates that the company's valuation is commensurate with its associated level of risk. Estimating intrinsic value is subject to variation in computations and valuation methods such as the Free Cash Flow to Equity (FCFE), the Gordon Growth Model, and the Discounted Cash Flow (DCF). The sensitivity study demonstrates the impact of variations in growth rates on value results. Moreover, the price multiples provide intriguing insights. Based on an analysis of the price-to-earnings (P/E) ratios, it can be inferred that Unilever is currently trading at a justifiable valuation concerning its earnings, both in terms of historical performance and future projections. In contrast, the P/B (Price-to-Book) and P/S (Price-to-Sales) ratios exhibit substantially elevated levels, suggesting the market assigns a premium valuation to the company's assets and sales.

In summary, Unilever demonstrates characteristics of a resilient and efficiently governed corporation, consistently earning profits and effectively leveraging its resources. The various valuation methods yield a spectrum of estimations, emphasising the inherent ambiguity involved in forecasting future performance. Based on the observed P/B and P/S ratios, the market assigns a premium to Unilever's assets and sales, indicating recognition of its robust brand presence and market standing. Unilever may present a viable investment opportunity for potential investors due to its consistent financial success and robust brand recognition.

References

d'Amico, G. and De Blasis, R., 2020. A review of the dividend discount Model: from deterministic to stochastic models. Statistical Topics and Stochastic Models for Dependent Data with Applications, pp.47-67.

Fernandez, P., de Apellániz, E. and F Acín, J., 2020. Survey: Market risk premium and risk-free rate used for 81 countries in 2020.

GlobalData (2023) Unilever PLC Company Profile - Overview, GlobalData. Available at: https://www.globaldata.com/company-profile/unilever-plc-gd33882/# (Accessed: 27 August 2023).

Huy, D.T.N. and Hang, N.T., 2021. Factors that affect Stock Price and Beta CAPM of Vietnam Banks and Enhancing Management Information System–Case of Asia Commercial Bank. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2), pp.302-308.

Johnson & Johnson (2012) Johnson & Johnson Annual Report 2012. Available at: https://www.sec.gov/Archives/edgar/data/200406/000020040613000038/ex13-form10xk20121230.htm#sCD848DFEBADDA7733AE0931F2B447B47 (Accessed: 27 August 2023).

Johnson & Johnson (2013) Johnson & Johnson Annual Report 2013. Available at: https://www.annualreports.com/HostedData/AnnualReportArchive/j/NYSE_JNJ_2013.pdf (Accessed: 27 August 2023).

Johnson & Johnson (2014) Johnson & Johnson Annual Report 2014. Available at: https://www.annualreports.com/HostedData/AnnualReportArchive/j/NYSE_JNJ_2014.pdf (Accessed: 27 August 2023).

Johnson & Johnson (2015) Johnson & Johnson Annual Report 2015. Available at: https://www.annualreports.com/HostedData/AnnualReportArchive/j/NYSE_JNJ_2015.pdf (Accessed: 27 August 2023).

Johnson & Johnson (2016) Johnson & Johnson Annual Report 2016. Available at: https://www.annualreports.com/HostedData/AnnualReportArchive/j/NYSE_JNJ_2016.pdf (Accessed: 27 August 2023).

Laitinen, E.K., 2019. Discounted Cash Flow (DCF) as a measure of startup financial success.

London Stock Exchange (2023) London Stock Exchange: Unilever PLC, London Stock Exchange | London Stock Exchange. Available at: https://www.londonstockexchange.com/stock/ULVR/unilever-plc/company-page (Accessed: 27 August 2023).

MarketWatch (2023) UL stock price: Unilever PLC ADR stock quote (U.S.: NYSE), MarketWatch. Available at: https://www.marketwatch.com/investing/stock/ul (Accessed: 27 August 2023).

Mordorintelligence (2023) Personal Care Industry Analysis - market overview, Personal Care Industry Analysis - Market Overview. Available at: https://www.mordorintelligence.com/industry-reports/global-beauty-and-personal-care-products-market-industry (Accessed: 27 August 2023).

Mordorintelligence (2023a) Home care market - size, Industry Overview & Growth, Home Care Market - Size, Industry Overview & Growth. Available at: https://www.mordorintelligence.com/industry-reports/home-care-market (Accessed: 27 August 2023).

Mordorintelligence (2023b) Snack food industry - size, share, trends, analysis, Snack Food Industry - Size, Share, Trends, Analysis. Available at: https://www.mordorintelligence.com/industry-reports/snack-food-market (Accessed: 27 August 2023).

Nestle (2012) Nestle Annual Report 2012. Available at: https://www.nestle.com/sites/default/files/asset-library/documents/library/documents/financial_statements/2012-financial-statements-en.pdf (Accessed: 27 August 2023).

Nestle (2013) Nestle Annual Report 2013. Available at: https://www.nestle.com/sites/default/files/asset-library/documents/library/documents/annual_reports/2013-annual-report-en.pdf (Accessed: 27 August 2023).

Nestle (2014) Nestle Annual Report 2014. Available at: https://www.nestle.com/sites/default/files/asset-library/documents/library/documents/financial_statements/2014-financial-statements-en.pdf (Accessed: 27 August 2023).

Nestle (2015) Nestle Annual Report 2015. Available at: https://www.nestle.com/sites/default/files/asset-library/documents/library/documents/financial_statements/2015-financial-statements-en.pdf (Accessed: 27 August 2023).

Nestle (2016) Nestle Annual Report 2016. Available at: https://www.nestle.com/sites/default/files/asset-library/documents/library/documents/financial_statements/2016-financial-statements-en.pdf (Accessed: 27 August 2023).

Pramono, E.S., Rudianto, D., Siboro, F., Baqi, M.P.A. and Julianingsih, D., 2022. Analysis investor index Indonesia with capital asset pricing model (CAPM). Aptisi Transactions on Technopreneurship (ATT), 4(1), pp.35-46.

Procter & Gamble (2012) Procter & Gamble Annual Report 2012. Available at: https://www.sec.gov/Archives/edgar/data/80424/000008042412000063/fy2012financialstatementsf.htm (Accessed: 27 August 2023).

Procter & Gamble (2013) Procter & Gamble Annual Report 2013. Available at: https://www.sec.gov/Archives/edgar/data/80424/000008042413000063/fy201310kannualreport.htm (Accessed: 27 August 2023).

Procter & Gamble (2014) Procter & Gamble Annual Report 2014. Available at: https://www.sec.gov/Archives/edgar/data/80424/000008042414000057/fy201410kannualreport.htm (Accessed: 27 August 2023).

Procter & Gamble (2015) Procter & Gamble Annual Report 2015. Available at: https://www.sec.gov/Archives/edgar/data/80424/000008042415000070/fy141510-kreport.htm (Accessed: 27 August 2023).

Procter & Gamble (2016) Procter & Gamble Annual Report 2016. Available at: https://www.sec.gov/Archives/edgar/data/80424/000008042417000047/fy161710-kreport.htm#s2E98B76251D20F1E81D020CCF8276B17 (Accessed: 27 August 2023).

Reckitt Benckiser Group (2012) Reckitt Benckiser Group Annual Report 2012. Available at: https://www.reckitt.com/media/ikhnbjo3/rb-annual-report-2012.pdf (Accessed: 27 August 2023).

Reckitt Benckiser Group (2013) Reckitt Benckiser Group Annual Report 2013. Available at: https://www.reckitt.com/media/dptfftbw/rb-annual-report-2013.pdf (Accessed: 27 August 2023).

Reckitt Benckiser Group (2014) Reckitt Benckiser Group Annual Report 2014. Available at: https://www.reckitt.com/media/vrcl1kmz/rb-annual-report-2014-1.pdf (Accessed: 27 August 2023).

Reckitt Benckiser Group (2015) Reckitt Benckiser Group Annual Report 2015. Available at: https://www.reckitt.com/media/rofnrics/rb-annual-report-2015_final.pdf (Accessed: 27 August 2023).

Reckitt Benckiser Group (2016) Reckitt Benckiser Group Annual Report 2016. Available at: https://www.reckitt.com/media/sx1dgqke/rb-annual-report-2016-no-spine.pdf (Accessed: 27 August 2023).

Statista (2023) Cosmetics & Personal Care, Statista. Available at: https://www.statista.com/markets/415/topic/467/cosmetics-personal-care/#insights (Accessed: 27 August 2023).

Statista (2023) Global: Food Market Revenue 2018-2028, Statista. Available at: https://www.statista.com/forecasts/1243605/revenue-food-market-worldwide (Accessed: 27 August 2023).

Statista (2023b) Food - worldwide: Statista market forecast, Statista. Available at: https://www.statista.com/outlook/cmo/food/worldwide (Accessed: 27 August 2023).

Statista (2023c) Snack Food - worldwide: Statista market forecast, Statista. Available at: https://www.statista.com/outlook/cmo/food/confectionery-snacks/snack-food/worldwide# (Accessed: 27 August 2023).

Sutjipto, E., Setiawan, W. and Ghozali, I., 2020. Determination of Intrinsic Value: Dividend Discount Model and Discounted Cash Flow Methods in Indonesia Stock Exchange. Eddy Sutjipto, Wawan Setiawan and Imam Ghozali, Determination of Intrinsic Value: Dividend Discount Model and Discounted Cash Flow Methods in Indonesia Stock Exchange, International Journal of Management, 11(11).

Unilever PLC (2012) Unilever Annual Report 2012. Available at: https://www.unilever.com/files/92ui5egz/production/61ebc6542e967e6fb5a8d5ee05a79238c8f6e4f7.pdf (Accessed: 27 August 2023).

Unilever PLC (2013) Unilever Annual Report 2013. Available at: https://www.unilever.com/files/92ui5egz/production/57d96b7700473ad2f70167a24fdfd425ee960b92.pdf (Accessed: 27 August 2023).

Unilever PLC (2014) Unilever Annual Report 2014. Available at: https://www.unilever.com/files/92ui5egz/production/bff0a3b0727b0222fe5226f1b052639708cab2c3.pdf (Accessed: 27 August 2023).

Unilever PLC (2015) Unilever Annual Report 2015. Available at: https://www.unilever.com/files/92ui5egz/production/ac9c917a9f639cf28d9421f6d7dcfe45733fdf23.pdf (Accessed: 27 August 2023).

Unilever PLC (2016) Unilever Annual Report 2016. Available at: https://www.unilever.com/files/origin/79524cdba4e993f9fd83a5d652c2c62ab46a55e6.pdf/unilever-annual-report-and-accounts-2016.pdf (Accessed: 27 August 2023).

Unilever PLC (2023) At a glance, Unilever. Available at: https://www.unilever.com/our-company/at-a-glance/# (Accessed: 27 August 2023).

Unilever PLC (2023) Our Company, Unilever. Available at: https://www.unilever.com/our-company/our-approach/

Xu, J., 2022, December. Advantages and Disadvantages of Dividend Discount Model and Better Alternatives. In 2022 International Conference on mathematical statistics and economic analysis (MSEA 2022) (pp. 456-461). Atlantis Press.

Yahoo!Finance (2023) Unilever plc (UL) stock price, news, Quote & History, Yahoo! Finance. Available at: https://finance.yahoo.com/quote/UL/ (Accessed: 27 August 2023).

Ycharts (2023) Unilever PS Ratio. Available at: https://ycharts.com/companies/UL/ps_ratio# (Accessed: 27 August 2023).

Would you like to schedule a callback?

Send us a message and we will get back to you

Highlights

Earn While You Learn With Us

Confidentiality Agreement

Money Back Guarantee

Live Expert Sessions

550+ Ph.D Experts

21 Step Quality Check

100% Quality

24*7 Live Help

On Time Delivery

Plagiarism-Free

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU