MANM376 International Finance Project Report Sample

Requirements:

The assessment is designed to test your ability to conduct and report an independent study, applying the principles and methods learned in the Cases in International Finance module.

You have been provided with three international finance-related projects. You can choose one, analyseusing the questions provided in this document and submit a project report. Alternatively, you canidentify a topic area of your interest and select an international finance-related case that you wish todevelop further.

Each project should have the following structure:

1. Title: You should include the title of the case with your student code

2. Executive summary: You should include an overview of your report.

3. Introduction: You should describe the case, highlight the points which are important in your view and answer the main question briefly.

4. Main analysis: You should provide your logical arguments here.

5. Conclusion: You should conclude the case, briefly summarise your main analysis and provide future recommendations.

6. References: Please use Harvard referencing style to cite references.

You must submit an essay with at least 5,000 words in length, excluding the references and appendices.

Project questions

Project 1: LVMH’s offer to purchase Tiffany & Co.

Please critically analyse the project and include the answer to this main question:

• Should LVMH acquire Tiffany? Is the deal good for Tiffany?

The following subquestions may help you answer the above main question:

• How similar are the businesses of LVMH and Tiffany?

• What are the benefits and risks for LVMH and Tiffany after the acquisition?

• Discuss LVMH and Tiffany’s potential future development after the acquisition.

• Calculate the intrinsic value of Tiffany and evaluate the fairness of the offer.

Project 2: Edita Food Industries’s IPO decision

Please critically analyse the project and include the answer to this main question:

• Should Edita go public? Will an IPO help finance its new investments?

The following subquestions may help you answer the above main question:

• What are the advantages and disadvantages of an IPO, compared with borrowing?

• Analyse the potential of the Egyptian Stock Exchange (EGX) for newcomers in the food and beverage sector.

• Assess the benefits and risks of getting listed on a foreign exchange, e.g., London Stock Exchange (LSE).

• How can Edita manage foreign exchange risk when purchasing its raw materials?

Project 3: Tata Steel’s capital structure decision

Please critically analyse the project and include the answer to this main question:

• How to determine the optimal capital structure for Tata Steel? What is the interaction between its cost of capital, capital structure, and business strategy?

The following subquestions may help you answer the above main question:

• Discuss the background and analyse the financial performance of Tata over the last few years.

• What are the factors that need to be considered for assessing the optimal financial leverage?

• Evaluate the potential methods of reducing financial leverage.

• How does the capital structure relate to the business strategy of Tata Steel?

Remember that all questions in the projects can be open to some extent, i.e., there are no correct/model answers. Your analysis is more important than your answer to a specific question. In your analysis, the logical arguments should be coherent.

Please focus your analysis on the main question. The sub-questions are provided to help you analyse the project better. You do not need to answer all the sub questions. It is up to your decision which sub- questions you wish to address. You do not need to limit yourself to answering the given sub-questions. Please feel free to use any resources/questions you think will help analyse the case better.

Solution

Project 1

LVMH’s offer to purchase Tiffany & Co.

Introduction

This case study examines LVMH's attempt to acquire the prestigious luxury jewelry company Tiffany & Co. The report evaluates the acquisition's possible advantages and strategic fit. With Tiffany's well-known brand and LVMH's intention to increase its luxury goods, there is potential for product diversification. While there are benefits like increased financial resources, global reach, and synergies, there are also difficulties to be overcome such as maintaining brand identity and cultural alignment. The examination also emphasizes shareholder impact, the competitive environment, and CEO opinions. Despite LVMH's superior market position, research highlights importance of preserving Tiffany's distinctive identity throughout integration. Potential advantages of an idea, such as market access and synergy, must be balanced against difficulties like brand preservation. In luxury market, where managing brand identity and utilizing synergies is essential for successful acquisitions, this case study demonstrates complexities of strategic decisions.

Main Analysis

Analysing different facets of both businesses, the luxury industry, as well as potential advantages and hazards of acquisition, is necessary when determining whether LVMH should purchase Tiffany & Co. According to the report, LVMH's acquisition of Tiffany could be strategically advantageous if done correctly. Tiffany's development prospects may be improved by LVMH's experience in managing its global footprint, luxury brands, and cash availability (da Silva, 2022). To make sure that deal is successful, there are some risks and problems that must be carefully controlled. Critical factors to take into consideration include protecting Tiffany's distinctiveness and maintaining fair valuation for university assignment help.

• Similarity

Tiffany and LVMH both work in luxury goods sector, although their main areas of interest are different. Broad luxury corporation, LVMH has a large portfolio of products in many luxury categories, including watches, fragrances, leather goods, wine, and spirits (Dong, Hui and Xia, 2022). Tiffany, on the other hand, specializes in high-end accessories and jewelry. The largest luxury corporation in the world, LVMH, is active in many industries, including those of wine and spirits, apparel and leather goods, cosmetics and fragrance, jewelry and watches, and selective retailing (Agrawal et al., 2022). However, Tiffany is best renowned for its designer jewelry and expensive accessories.

• Differences

Each brand under the LVMH umbrella has a distinct character and target market. Famous brands like Christian Dior, Louis Vuitton, Bulgari and Dom Pérignon, are among members of this organization, which sells everything from watches and champagne to clothing and accessories. LVMH's broad portfolio enables it to meet preferences of a variety of luxury consumers and broaden its reach in numerous markets (Agrawal et al., 2022). On the other side, Tiffany sells high quality jewellery, which is a completely different product range.

• SWOT Analysis:

LVMH:

.png)

.png)

Tiffany & Co

.png)

Business valuation

Among the several elements that might cause an acquisition to fail. One critical feature is an overly optimistic estimation of economies of scale (U Steger, C Kummer,2007). These estimations are based on the techniques listed below.

-Net Asset Method: This method involves moving balance-sheet items such that all operational items are on the left and all financial items are on the right. This strategy can serve as the foundation for valuing a firm. This strategy is beneficial in the event of a liquidation. It produces better results for asset-intensive businesses.

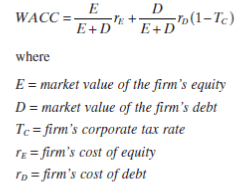

The N.A approach presents a problem. It does not consider a company's potential. Because intangible assets are more prevalent in service-related businesses. As a result, estimating replacement costs is challenging.-Cash Flow Based Model: it seeks to evaluate the business based on the present value of the firm's future expected free cash flow (FCF) discounted at the WACC. The following is the process for estimating WACC:

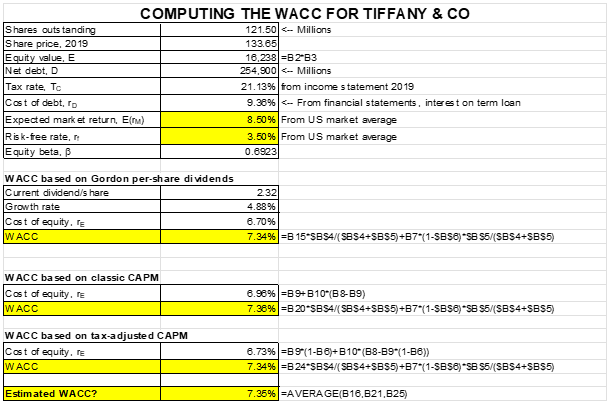

As mentioned above WACC have five components. To find the value for Tiffany calculations are as follows:

Market Value of Equity = number of shares multiply by market price of share at that date

.png)

.png)

It is believed that the current year debt values are the same as the debt values in 2019, making this a less risky investment.

RD is the cost that the principal must pay for each additional dollar borrowed. It is usually done based on the firm's average cost. The usual issue with this strategy is that it conflates past debt costs with future debt costs.

.png)

Tax rate is being calculated from the income statement and it is assumed that the rate of tax in 2019 will be remain same for further years as well.

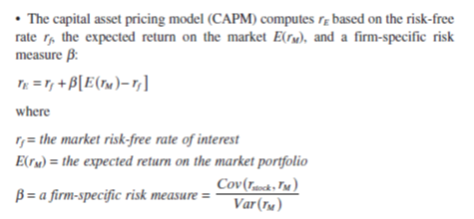

GGM (Gordon's growth model) and CAPM (Capital asset pricing model) can be used to calculate the cost of equity. GGM is dependent on various assumptions, such as the dividend growing at the same rate it would increase in the future and the proportion of earnings reinvested, which do not demonstrate the present business risk. As a result, it is preferable to compute Ke using CAPM since it incorporates systematic risk (both business and financial risk).

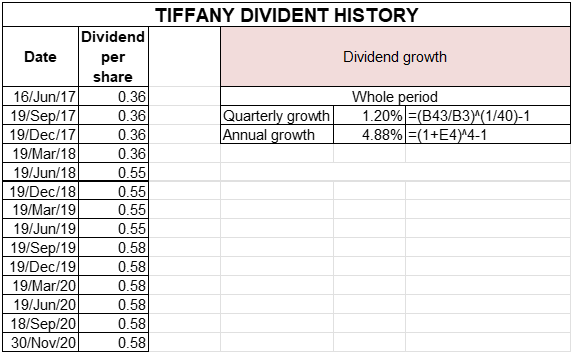

To find the growth rate the value are as follows:

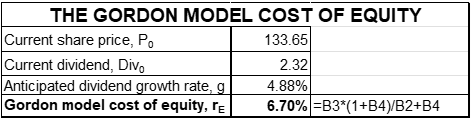

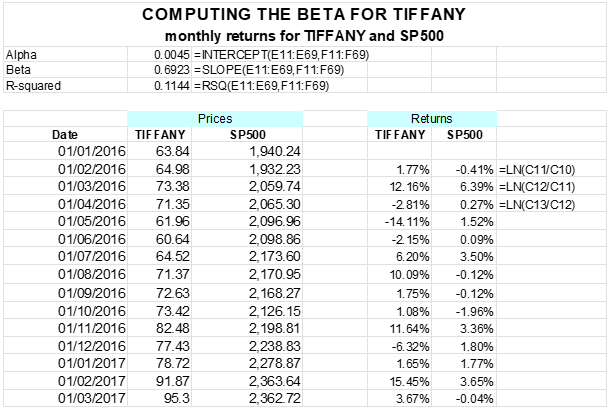

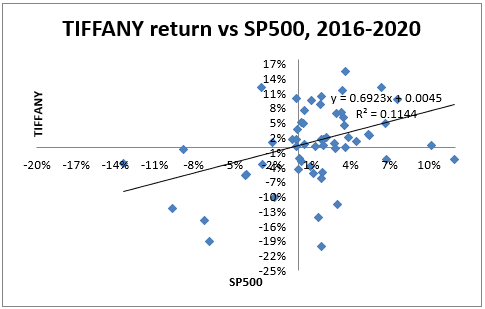

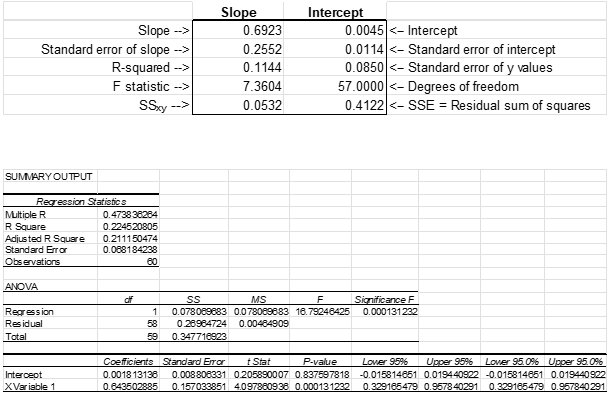

Re for Tiffany & co. is 6.7% as per GGM. As this rate doesn’t include the business risk to calculate the business risk the value of Beta is being calculated with the comparison of Tiffany share and index SP500 as follows:

As from the above calculations the value of Beta is 0.6923 which is less then 1. Hence it also states that the business is less risky.

The WACC of a company depend upon it capital structure of a company the WACC of Tiffany & co. using GGM and CAPM are as follows:

In the above calculation it is assume the risk-free rate is assumed to be the same as the treasury bill of US and expected market return of a company is the same as the industry market average. The WACC which is used for the valuation of a company is an average of WACC using GGM and CAPM with and without Tax.

FREE CASH FLOW MODEL

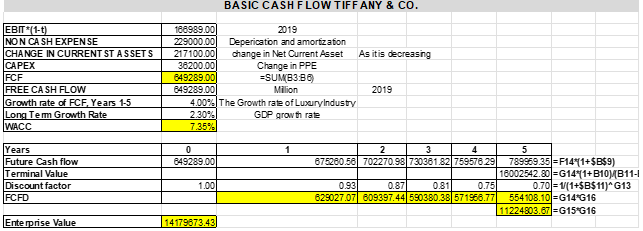

The FCF value is derived from the Unlevered Free Cash Flow before the influence of cash and debt. After then, the impact of debt and cash will be equalised. It is thought that the amount of FCF reflects the business's usual capability. The growth rate is the industry rate, which is supposed to be linked with the business rate. The long-term growth rate is the GDP rate, and re, rd remains constant. DCF focuses not just on the company's prospects but also on its operational flow. To calculate FCF is as follows:

After applying all the values to find Enterprise Value by using FCFD is as follows.

From the above calculation the value of the Tiffany is & Co. is 14.17 billion. Where as LVMH value the company at 15.8 Billion, was overpriced by Approximately 9.5%. where as the first offer which was made by the LVMH was near to the company current value to acquire Tiffany & Co.

LVMH purchasing Tiffany & Co. and improving the company's cashflow and growth rate might cause Tiffany & Co. to be valued higher and justify the purchase. To see if DCF analysis results are consistent with our Comparable Company Analysis results, indicating that Tiffany & Co.'s shares and ultimate acquisition were expensive is in the following heading.

Comparable Analysis:

Comparable Analysis method is used to evaluate the fairness of the offer for its stakeholder to assess the correct valuation of the target company. It incorporates the effect of market reflect higher price if the shares are bull and lower if the share are bear (Kaplan and Ruback, 1996). To do the comparative analysis we will compare the competitors with same industry and their financial ratios with target company.

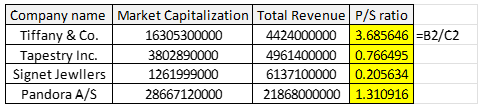

For the purpose of this analysis this report will focus on the businesses operating in the same industry. To do the comparison companies which will be use for the comparison are Pandora CPH, Signet Jewellers Ltd and Tapestry Inc. The comparison will be done by financial ratios of the above companies for the financial year 2019 when the LVMH had made their first offer. The analysis of the ratios are as follows:

Price to sale ratio:

This ratio will focus on how much market values the company for each dollar of the company sales. This ratio is effective for growth in stock valuation.

P/S Ratio=MVS/SPS

As we can see the price of Tiffany is overpriced again in comparison to its competitors whereas in ratios the hight P/S is for Pandora and lowest is for Signet Jewellers. For the time period under consideration if the Tiffany & Co. P/S is near to its competitors then ideal price would be

=$134.2/Share x ( 1.495/3.685) = $54.365

As from the above calculation the price of the company is $ 54.365 which is 58.65% less than the offer price of USD 131.5.

PRICE TO EARNING RATIO:

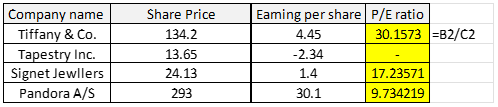

P/E ratio describe the relation of stock earnings and its price. High P.E explains the possibility of high stock price in relevance to its earnings. A low P.E might indicate that the stock price is low relative to earnings.

P/E = Share price / Earnings

By the end of 2019 the P/E of Tiffany & Co. is 30.157 whereas for its competitors highest P/E is 17.23 for Signet jewellers. It is important to highlight that Tapestry earning as in negative here they don’t have any P/E. By using the closest value of its competitor the share price of Tiffany & Co. should have been

$134.2 x (17.23 / 30.157) = $76.67

Which is about 42 % lower then the Market Price for its year 2019 and is also about 41% lower then the final acquisition price 131.5 which is paid by LVMH.

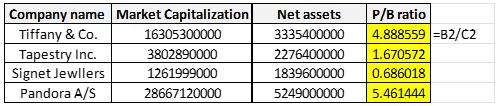

Price to Book Ratio:

PBR is also another financial valuation metric that is used to do the comparative analysis of any company by using the book value of the company. In other words, the book value is when total net assets of company are deducted from the total liabilities of the company. To calculate the price to book ratio it is as follows:

PBR = Market Capitalization / Net assets

In doing the comparative as can see the Tiffany & Co Net asset to book value is 4.89 for its share price. The company's nearest rivals have a mean P/B ratio of 3.18, with a median of 3.28. Once again, the results of another financial statement, this time focusing on a firm's balance sheet, demonstrate that Tiffany & Co. was expensive in comparison to its competitors. It would have been at if it had been priced according to the mean ratio of its nearest rivals.

$134.2 x (3.18/4.89) = $87.27

The stated price is 35% cheaper than the current market price and 33.63% lower than the USD 131.5 paid by LVMH to buy Tiffany & Co.

LVMH acquiring Tiffany & Co.

The cornerstones of LVMH's financial strategy are acquisitions and mergers. The conglomerate's most recent acquisition, Tiffany & Co., a titan in the premium jewellery and specialised retail industries, was finalised at the beginning of 2021. Knowing Tiffany & Co.'s history is essential for understanding the factors that led to the acquisition. The well-known company is based in New York City and sells a wide range of goods, including leather goods, sterling silver jewellery, porcelain, crystal, stationery, and timepieces. As of 2019, Tiffany was a multinational enterprise with 326 stores across the world. Countries including Japan, the United States, and Canada as well as territories in Europe, Latin America, and Pacific Asia contain these locations. Tiffany has established itself as one of the most well-known and enduring brands, in part because to its distinctive hue and engagement ring in the shape of a diamond.

Source: “Wealth creation by M&A activities in the luxury goods industry”. European Business School, Department of Finance. French conglomerate tried to defend its choice by also referencing letter from minister of international affairs of France, in which he urged delaying operation due to American threats to tax French goods (Alvarez, 2023). Tiffany retaliated by filing a lawsuit in Delaware against LVMH, claiming that the conglomerate wanted to deliberately impede the process of obtaining antitrust permits for the acquisition in order to manipulate price.

Benefits of Acquisition

Facts and history have demonstrated that LVMH, despite its dismal accomplishments, has a laudable ability to restore brands. Given its significance and the difficulties it was facing, Tiffany was the ideal target for the French firm (Jokinen, 2023). Latter had always been upbeat about Tiffany's potential and was sure he could assist the business in overcoming its difficult situation and lost possibilities.

Jewellery Portfolio Diversification and Strengthening: LVMH's footprint in the jewelry industry was not as strong as it was in other high-end markets. Enhancing LVMH's global presence in the jewelry business was made possible by the strategic opportunity presented by acquisition of Tiffany & Co. (Paul, 2023).

Access to U.S. Market: Tiffany's dominant position in high-end American market would give LVMH chance to enter a market it had not yet fully entered. Through acquisition of Tiffany & Co., LVMH gained access to affluent U.S. market, expanding its geographic reach beyond its traditional strengths (Dalla Pace, 2021). Tiffany & Co. is well-known brand.

Source: “Group key figures” - LVMH investor’s webpage

Appealing for Younger Consumers: In order to attract younger people who may subsequently become customers of LVMH's expensive brands as their purchasing power develops, LVMH sought to exploit Tiffany's relatively more inexpensive offerings. Through Tiffany, LVMH deliberately developed long-lasting connections with customers across luxury spectrum. Tiffany captured the interest of younger people.

Growth Potential in Global Jewellery Industry: Given the high entry barriers in luxury jewellery market and profit potential and predicted growth global jewellery market, LVMH may have large revenue prospects. Given high entry hurdles to the luxury jewelry industry and predicted expansion and profitability for the global jewelry market, LVMH expects to acquire access to significant revenue potential.

Access to money: Tiffany would have easier access to money at more affordable rates thanks to LVMH's size and financial stability, expansion and potentially enabling growth. Tiffany's partnership with LVMH might improve its access to finance resources at better terms because of LVMH's enormous scale and strong financial position (Tocha, 2022).

• Benefits and risks of LVMH

Benefits for LVMH

Diversification: By entering the jewelry market with Tiffany, LVMH can diversify its portfolio even more. LVMH's ability to adapt is boosted by addition of a well-known jewelry company like Tiffany, enhancing resilience of its entire business strategy (Lojacono and Pan, 2021).

Market Access: Tiffany's long-standing position in the U.S. luxury market gave LVMH a competitive edge in this valuable industry (Dudia and Mathur, 2022). Through this acquisition, LVMH was able to benefit from Tiffany's well-known brand and devoted following, strengthening its entry and development into American luxury market and giving it better competitive edge.

Benefits for Tiffany

Access with Resources: Tiffany has access to the knowledge, skills, and global network of LVMH. Tiffany capitalizes on LVMH's tremendous resources, knowledge, and global reach. Through this relationship, there are chances for sharing best practices, innovation, and operational benefits.

Product Innovation: Working together with different LVMH brands may result in development of new products and an increase in innovation. Collaboration among Tiffany and different LVMH companies can promote idea-cross-pollination, resulting in the development of novel and distinctive items that satisfy range of consumer tastes.

Risks for LVMH

Brand Integration: It is difficult to integrate Tiffany with LVMH's portfolio while maintaining Tiffany's own brand identity. Harmonizing Tiffany's distinctive brand identity with LVMH's broad portfolio is difficult task.

Culture and Management: Ensuring a seamless transfer and alignment for management styles and cultural norms. Maximizing advantages of purchase and enabling effective decision-making across merged organizations will depend critically on eliminating any differences and encouraging cohesive, collaborative environment (Bates et al., 2023).

Risks for Tiffany

Loss of Independence: Upholding Tiffany's distinctive history and reputation despite being part of larger conglomerate. Concerns regarding Tiffany's loss of autonomy and its capacity to uphold distinctive identity and heritage it has developed over a long history may arise in wake of company's acquisition by LVMH.

Integration of cultures: Making sure Tiffany and LVMH have similar management philosophies and corporate cultures. To enable seamless integration, Tiffany and LVMH's business cultures must be brought into agreement. It can affect employee morale, teamwork, and overall company performance by aligning management practices.

• Future Potential Developments Following the Acquisition

Post-acquisition

Tiffany may be able to aggressively diversify its product offerings, fund marketing initiatives, and penetrate new markets thanks to LVMH's extensive resources. Tiffany might profit from LVMH's investment in its marketing, expansion, and innovation plans. Well-established presence of LVMH in numerous locations provides priceless market knowledge, distribution channels, and insights (Pereira, 2020). Tiffany's international expansion might be accelerated by the merged firm, particularly in emerging areas, by utilizing LVMH's extensive global network.

Benefits of Acquisition

Increased Market Access: Tiffany & Co. may have more access to worldwide markets thanks to LVMH's substantial global footprint and distribution networks, especially in areas where LVMH is well-established. A considerable opportunity for expedited market expansion is provided by Tiffany & Co.'s prospective access to LVMH's extensive global network.

Brand synergy: LVMH's expertise in overseeing luxury brands may help to improve Tiffany's brand reputation and consumer attractiveness. Tiffany's offerings might be revitalized and modernized with the help of LVMH's experience in retail operations and marketing design (Roggeveen et al., 2021).

Risks and Considerations

Loss of Independence: Tiffany's personality and distinctiveness can be lost if joins a larger company. To keep the brand's devoted following, it will be essential to maintain its originality. Brand's distinguishing qualities, legacy, and values must persist to keep its loyal customer base. Success will depend on finding a balance between utilizing conglomerate's resources and maintaining Tiffany's identity.

Cultural Alignment: It can be difficult to combine two different business cultures. A successful merger will depend on the LVMH along with Tiffany teams working in harmony and cooperation. Open communication, respect for one another, and common goals are necessary for seamless integration (Satka et al., 2023). Collaboration between Tiffany and LVMH teams will be essential for managing culture differences, establishing unified strategy, and ensuring success of combined company.

Regulatory permission: In some nations, acquisition can need regulatory permission. The acquisition schedule can be impacted if obtaining these clearances takes longer than expected or is rejected. If process of acquiring required permits takes longer than expected or should certain regulatory authorities reject merger, necessitating revisions to the broader integration strategy, acquisition's development may be hampered.

• Calculating intrinsic value

Projecting future cash flows and decreasing them compared with current value are both necessary steps in determining company's intrinsic worth. Let's utilize a straightforward DCF (Discounted cash flow) model for estimating Tiffany's intrinsic worth.

Projected Upcoming Cash Flows: Tiffany's anticipated future cash flows. For this example, let's assume that Tiffany's anticipated cash flows for the following five years are the following (in millions of USD):

(Refer Appendix – I)

Tiffany & Co.'s cash flows have increased over past five years; this could be for a number of reasons, including:

- Tiffany & Co. may have increased cash inflows as a result of selling more goods or services if its revenue growth is constant over time.

- Higher net cash flows could arise from greater profitability brought on by effective expense reduction or effective cost management.

- Sales and revenue may rise as a result of expanding the client base, introducing new items, or entering new markets.

- If Tiffany & Co. gradually increases the cost of its goods, it can see more sales and cash flows.

- Increasing efficiency and streamlining processes can increase cash flows and profitability.

- Sales and revenue of a corporation can be impacted by patterns in consumer spending and overall economic growth.

Evaluating reasonableness of LVMH's acquisition offer for Tiffany & Co.

Market value vs. the offer price: When Tiffany's share price recently fluctuated between USD 88 and USD 98, LVMH's original offer of USD 120 each share was viewed as a premium. The management of Tiffany, however, thought that this offer undervalued business. As a result of successive counteroffers, offer price was raised from USD 135 for each share, which constituted a significant premium above the opening trading range. The rising proposals show LVMH's commitment to acquiring Tiffany.

Strategic Fit: With this acquisition, LVMH would have a greater footprint in the jewelry industry and its first significant non-fashion brand United States. This strategic match supports LVMH's objective of diversifying luxury offerings in its portfolio.

Financial Strength: Under direction of CEO Alessandro Bogliolo, Tiffany's financials reflect a comeback in net income. Although the company's operational costs and costs of products sold are substantial, its revenue and gross profit have grown. Bogliolo's emphasis on improving operational effectiveness and cutting expenses is clearly responsible for the increase in net income.

CEO's Point of View: CEO Alessandro Bogliolo stressed the value of maintaining Tiffany's legacy, product quality, and brand. This viewpoint is consistent with the notion that a company's success depends on how its target market perceives it. Bogliolo emphasizes the significance of preserving characteristics that have distinguished Tiffany for 182 years because he is aware that company's success depends on how its customers perceive it (Fraser, 2020).

Shareholder's Perspective: The initial offer was rejected by Tiffany's shareholders as being too low, demonstrating that they thought company was worth more than that. The increase in offer price that followed can reflect the shareholders' influence on discussions. This demonstrates impact of shareholders on negotiation process by forcing LVMH to re-evaluate and gradually increase offer price.

Competition: As biggest luxury company, LVMH's offer probably didn't face much opposition because of its dominance in sector. Few competitors could equal LVMH's dimensions, resources, and influence given company's dominance across several luxury sectors, potentially making it a strong contender to acquire Tiffany & Co.

Regulation: Since LVMH's offer remained unsolicited and there were no other proposals, regulatory obstacles could not have been as important. Regulatory obstacles may have been lowered by LVMH's unsolicited bid and the lack of competing alternatives (Peleg Mizrachi and Tal, 2022).

Conclusion

The possible LVMH takeover of Tiffany & Co. presents both strategic advantages and difficulties. Innovation and Tiffany's growth may benefit from LVMH's global resources and network, and Tiffany's distinctive brand identity is consistent with LVMH's plan to revitalize brands. The preservation of Tiffany's legacy while leveraging LVMH's advantages is essential for the integration to succeed. For post-acquisition success, cultural congruence and effortless collaboration are essential. The complementary nature of the two businesses can spur innovation and market growth. Cultural conformity and maintaining independence, however, present difficulties. Monitoring trends in market and establishing long-term plans are crucial as luxury sector changes. In conclusion, a well-executed acquisition can position Tiffany and LVMH as formidable forces in luxury market if it is led by brand preservation, customer attention, and strategic partnership.

Recommendations

- Both businesses have a great chance with acquisition to strengthen their positions in luxury market, particularly in the jewelry sector. Tiffany's diversification, expansion, and innovation ambitions are set to be fuelled by LVMH's enormous experience, financial support, and global connections.

- A crucial factor to take into consideration is how to maintain Tiffany's own brand identity while reaping rewards of partnership.

- For companies LVMH and Tiffany, proactive approach is essential. By using Tiffany's development potential and LVMH's expertise in reviving ailing brands, collaboration may forge more robust presence in the premium market (Johnson and Misiaszek, 2022).

- Both businesses are dedicated to providing outstanding customer experiences. This unifying philosophy can be used to forge synergies that will improve overall luxury shopping experience and encourage repeat business.

- Due to the fluid nature of the luxury industry, ongoing attention must be paid to shifting market trends, consumer preferences, and economic conditions. Maintaining relevance and competitiveness will depend on being flexible and adaptable.

- In the post-acquisition phase, efforts to harmonize management philosophies and corporate cultures are crucial. A successful integration will depend heavily on encouraging cooperation and understanding between parties.

- Compliance with legal requirements is essential. Legally sound and problem-free acquisition requires obtaining the required approvals and negotiating regulatory assessments.

- Innovation may be sparked by partnership between Tiffany and LVMH (Akpinar, Haapalainen and Skog, 2022). Joint efforts can open door for creation of novel goods, market approaches, and innovation, resulting in sustained growth and an edge over the competition.

References

Agrawal, G., Rathi, R., Garg, R. and Chhikara, R., 2022. Abundantly rare: changing consumer trends in the luxury market. Vision, Vol. 0 No. 0. doi, 10, p.09722629221104201. https://www.researchgate.net/profile/Rubal_Rathi2/publication/354923662_Abundantly_Rare_Changing_

Consumer_Trends_in_the_Luxury_Market/links/615c80615a481543a8874fbd/Abundantly-Rare-Changing-Consumer-Trends-in-the-Luxury-Market.pdf

Akpinar, M., Haapalainen, V. and Skog, N., 2022. An exploratory study on growth strategies in the jewelry retail industry. In From Globalization to Regionalization in a Time of Economic, Socio-Political, Competitive, and Technological Uncertainties: Current Issues and Future Expectations. Twenty Ninth World Business Congress. June 12-16, 2022 JAMK University of Applied Sciences Jyväskylä, Finland. International Management Development Association. https://www.theseus.fi/bitstream/handle/10024/780100/Article.pdf?sequence=1

Alvarez, N., 2023. Nothing in Life is Free: Franco-American Economic Relations and American Investment in Postwar France (1945-1969) (Doctoral dissertation). https://ir.vanderbilt.edu/bitstream/handle/1803/18263/NAlvarez%20Final%20Draft%20SIGNED%

20COVER%20SHEET.pdf?sequence=1

Bates, G., Le Gouais, A., Barnfield, A., Callway, R., Hasan, M.N., Koksal, C., Kwon, H.R., Montel, L., Peake-Jones, S., White, J. and Bondy, K., 2023. Balancing autonomy and collaboration in large-scale and disciplinary diverse teams for successful qualitative research. International Journal of Qualitative Methods, 22, p.16094069221144594. https://journals.sagepub.com/doi/pdf/10.1177/16094069221144594

da Silva, H.D.G., 2022. Diversification in the Personal Luxury Goods Industry: A Case Study of LVMH and its Peers Financial Performance and Mergers and Acquisitions Strategies. https://repositorio-aberto.up.pt/bitstream/10216/144767/2/588785.pdf

Dalla Pace, G., 2021. The Operation of Cross-Border Merger in the Luxury Industry. http://dspace.unive.it/bitstream/handle/10579/20578/989295-1267873.pdf?sequence=2

de Linos, M.S.D., 2020. THE INFLUENCE AND EVOLUTION OF THE LUXURY SECTOR. https://biblioteca.cunef.edu/files/documentos/TFG_Maria_Santo-Domingo_de_Linos.pdf

Dong, Z., Hui, R. and Xia, Y., 2022. Research on the investment value of LVMH-based on multiple valuation method. https://pdfs.semanticscholar.org/49d7/66deeb0222ba4173fd718ec586ae614becc5.pdf

Dudia, A. and Mathur, A., 2022. A STUDY OF LUXURY GOODS MARKET FOR EXPERIENTIAL MARKETING. BUSINESS ADMINISTRATION, p.91. http://www.busadmjnvu.org/AMRITA%20DUDIA%20&%20DR.%20ASHISH%20MATHUR.pdf

Fraser, C.A., 2020. Contextually Recommending Expert Help and Demonstrations to Improve Creativity. University of California, San Diego. https://search.proquest.com/openview/aa3dc0ebdc835528abc6456ec98016ae/1?pq-origsite=gscholar&cbl=18750&diss=y

Johnson, M. and Misiaszek, T., 2022. Branding that Means Business: Economist Edge: books that give you the edge (Vol. 1). Profile Books. https://books.google.com/books?hl=en&lr=&id=yPhYEAAAQBAJ&oi=fnd&pg=PT12&dq=By+using+Tiffany%27s+development+potential+and+

LVMH%27s+expertise+in+reviving+ailing+brands,+collaboration+may+forge+more+robust+presence+in+the+

premium+market.&ots=BSNb7VvUOx&sig=NB4GCtCsHNvBvRW61UWukRkrSF0

Jokinen, E., 2023. Sustainable actions adapted to luxury strategy: Case Bulgari, Tiffany & Co., Pomellato & Qeelin: A critical discourse analysis. https://osuva.uwasa.fi/bitstream/handle/10024/15534/UniVaasa_2023_Jokinen_Eerika.pdf?sequence=2&isAllowed=y

Kaplan, S. and Ruback, R., 1996. “The Market Pricing of Cash Flow forecasts: Discounted Cash Flow VS. The Method of Comparables”, Journal of Applied Corporate Finance, 8(4), pp 45-60.

Lojacono, G. and Pan, L.R.Y., 2021. Resilience of luxury companies in times of change. Walter de Gruyter GmbH & Co KG. https://books.google.com/books?hl=en&lr=&id=yQRGEAAAQBAJ&oi=fnd&pg=PR5&dq=LVMH%27s+ability+to+adapt+is+boosted+by+addition+

of+a+well-known+jewellery+company+like+Tiffany,+enhancing+resilience+of+its+entire+business+strategy.+&ots=S-ggsT7p4H&sig=FIzXg_B1eA0oTSgv1eGJtgZRKyo

LVMH. 2023. LVMH company - An operational and functional model – LVMH. Available at: https://www.lvmh.com/group/about-lvmh/model-lvmh/ (Accessed: 5 September 2023).

McMaster, M., Nettleton, C., Tom, C., Xu, B., Cao, C. and Qiao, P., 2020. Risk management: Rethinking fashion supply chain management for multinational corporations in light of the COVID-19 outbreak. Journal of Risk and Financial Management, 13(8), p.173.

Paul, J., 2023. MASSTIGE MARKETING: TEN ESSAYS. https://research.brighton.ac.uk/files/40900312/Brighton_Thesis_R3_merged.pdf

Peleg Mizrachi, M. and Tal, A., 2022. Regulation for promoting sustainable, fair and circular fashion. Sustainability, 14(1), p.502. https://www.mdpi.com/2071-1050/14/1/502

Pereira Jr, S., 2020. The Monument Brands: Examining Luxury Firm Investment in Cultural Legacy Programs (Doctoral dissertation, Southern New Hampshire University). https://search.proquest.com/openview/86bd9418d67bc8443769ab848f332390/1?pq-origsite=gscholar&cbl=18750&diss=y

Roggeveen, A.L., Grewal, D., Karsberg, J., Noble, S.M., Nordfält, J., Patrick, V.M., Schweiger, E., Soysal, G., Dillard, A., Cooper, N. and Olson, R., 2021. Forging meaningful consumer-brand relationships through creative merchandise offerings and innovative merchandising strategies. Journal of Retailing, 97(1), pp.81-98. https://www.sciencedirect.com/science/article/pii/S0022435920300889

Satka, Z., Ashjaei, M., Fotouhi, H., Daneshtalab, M., Sjödin, M. and Mubeen, S., 2023. A comprehensive systematic review of integration of time sensitive networking and 5G communication. Journal of Systems Architecture, 138, p.102852. https://www.sciencedirect.com/science/article/pii/S1383762123000310

Sothebys. 2018. Tiffany & Co.'s Brilliant History. Available at: https://www.sothebys.com/en/articles/tiffany-200-year-history (Accessed: 5 September 2023).

Steger, U. (2007) Why Merger and Acquisition (M&A) Waves Reoccur - The Vicious Circle from Pressure to Failure , Psu.edu. Available at: https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=1aae1bd348e9012c5eb527203358048e208ffd23 (Accessed: 05 September 2023).

Tocha, G.C., 2022. Shining bright like a diamond (Doctoral dissertation). https://run.unl.pt/bitstream/10362/144698/1/lvmh-equity-research---gabriel-tocha-and-jose-coutinho.pdf

Would you like to schedule a callback?

Send us a message and we will get back to you

Highlights

Earn While You Learn With Us

Confidentiality Agreement

Money Back Guarantee

Live Expert Sessions

550+ Ph.D Experts

21 Step Quality Check

100% Quality

24*7 Live Help

On Time Delivery

Plagiarism-Free

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU