FE7066 Data Analysis for Global Business Coursework Sample

Background

With the increasing disclosure of Corporate Social Responsibility (CSR)-related information, more and more Small and Medium-sized Enterprises (SMEs) are expected to establish internal mechanisms within their businesses that lead towards more sustainable behaviour, such as integrating CSR-related aspects into existing management control systems. A study was conducted in 2023 to examine the drivers of the existence of such CSR-related management control components and the corresponding effects on performance of SMEs in a country.

The study aims to provide an overview of the influencing factors that would drive the existence of CSR-related formal and informal controls at a given moment in time. This was based on legitimacy theory which argues that top-level managers’ perceived importance of CSR, stakeholder expectations and proactiveness influence the existence of CSR-related formal and informal controls. A questionnaire was used to collect data from a cross-industry design that included both small and medium-sized enterprises (SMEs), the questionnaire consists of 10 questions. The contents of the questions include the constructs of the theoretical model and additional measures, such as demographics and social desirability. Several steps were taken to ensure the reliability of the data such as a random sampling and extensive pre-testing with experts from a local economic development corporation as well as managers of companies within different industries. There were 1,938 SMEs in the country and 200 copies of the questionnaire were distributed to the top-level managers of selected samples of companies during the period from 15 th October to 15 th December 2023, 163 out of 200 completed questionnaires were returned. The feedback from these respondents was recorded in a MS Excel Spreadsheet.

Requirements

1. Use IBM SPSS Statistics or MS Excel Spreadsheet to analyse the primary data collected by this study.

2. Write a formal report of 1,000 words to evaluate the results from the study. A copy of the questions of this Questionnaire is attached. The data set in a MS Excel file is available from module Weblearn via Assessment Details.

Solution

1. Introduction

This report looks at the findings of a study done in 2023 that tried to find out what makes CSR-related management controls show up and how they affect the success of small and medium-sized businesses (SMEs). The study was done because CSR is becoming more important to small and medium-sized businesses. This study uses legitimacy theory to look into the factors that affect the appearance of official and informal rules related to CSR. These factors include how important top-level management thinks CSR is, what stakeholders expect, and how engaged people are.

2. Data Analysis and Interpretation

2.1 Demographic Analysis

.png)

Chart 1: Gender Distribution

(Source: Author)

Among the 163 responses received, 134 of top-level managers were male and just 29 were female, indicating a significant gender imbalance. Because of the possible lack of female viewpoints in developing CSR-related management controls, this gender disparity may affect how broadly applied the study's conclusions are. Hence, to know what variables impact sustainable business practices in SMEs, it is needed to fill the gender gap in leadership (Maida and Weber, 2022) (See Appendix 1).

2.2 Company and Industry Analysis

.png)

Chart 2: Employee number distribution across companies

(Source: Author)

The majority of the respondents (85) work for organisations with more than 500 employees, indicating that the survey is heavily skewed towards bigger enterprises in terms of company size (Q2). The study's results are not accurately applicable to smaller enterprises due to this distribution, which implies that the findings are more relevant to mid-sized and larger SMEs (See Appendix 2).

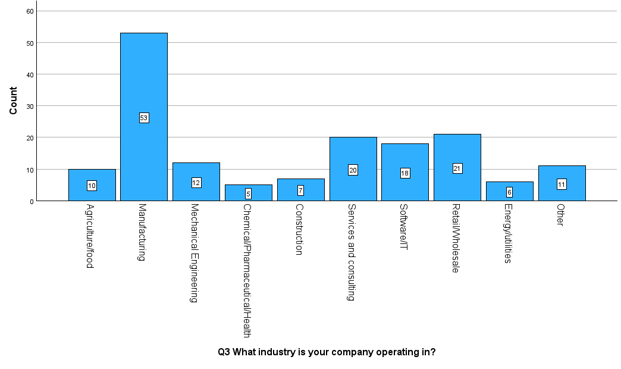

Chart 3: Distribution of industries

(Source: Author)

Results show a diverse range of industries when looking at industry variety (Q3), with manufacturing (53), services and consulting (20), and retail/wholesale (21) being the most prominent. A more thorough comprehension of CSR-related management controls across various economic sectors is made possible by this industrial variety, which also increases the study's external validity. However, it is a concern due to the extrapolating results from a single industry resulting in unequal distribution (Bhuiyan et al. 2022) (See Appendix 2).

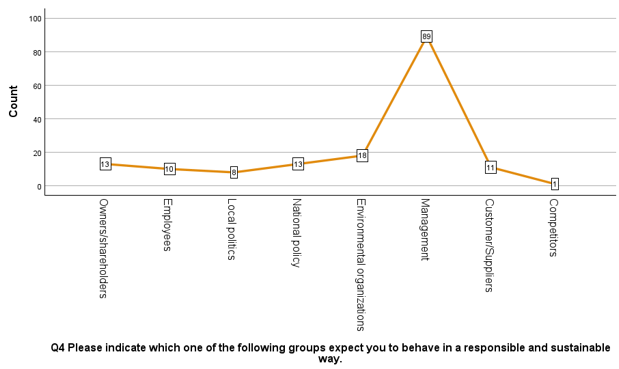

Chart 4: Stakeholder’s Expectations

(Source: Author)

Moreover, aspects of stakeholder expectations and management perspectives inside SMEs are also shed light on by the survey findings. When asked about the groups that demand responsible and sustainable behaviour (Q4), a large majority of respondents (89) stated that ‘management’ had such expectations. This highlights how important it is for SMEs to have strong internal incentives and strong leadership which impact their CSR activities (Kuzior et al. 2021). Furthermore, the acknowledgement of environmental organisations (18) emphasises the growing impact of outside parties on CSR standards (See Appendix 2).

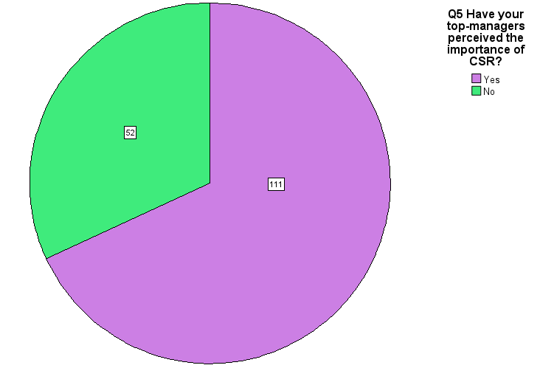

Chart 5: Stakeholder’s Expectations

(Source: Author)

The majority of senior managers (111) recognise the relevance of CSR when asked about their assessment of its value (Q5). This bodes well for SMEs' growing awareness of CSR as a key strategic priority. On the other hand, a large percentage of upper management may not be on the same page, as 52 of respondents said otherwise. In order to guarantee a harmonious and efficient integration of management controls connected to CSR, it is essential to resolve this disagreement. These results highlight the need of focused methods, particularly within internal management, to encourage a shared dedication to ethical and environmentally friendly company operations (Sendlhofer, 2020) (See Appendix 2).

2.3 CSR Related Management Control Systems Analysis

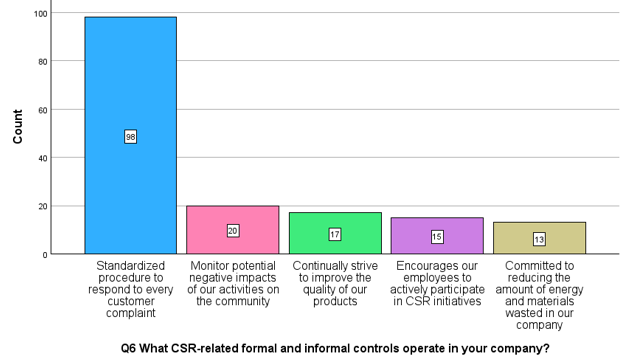

Chart 6: CSR Related Controls

(Source: Author)

The survey results for university assignment help show that regarding particular regulations (Q6), 98 of respondents support a standardised approach for client complaints. An emphasis on the client is central to this CSR strategy. A dedication to eliminating energy and material waste (13) and monitoring possible negative effects on the community (20) demonstrate environmental awareness, but to a lower level. The findings stress how important it is for SMEs to increase the scope of their CSR controls, encouraging a broader strategy for sustainability that takes social and environmental factors into account (Almashhadani, 2021) (See Appendix 3).

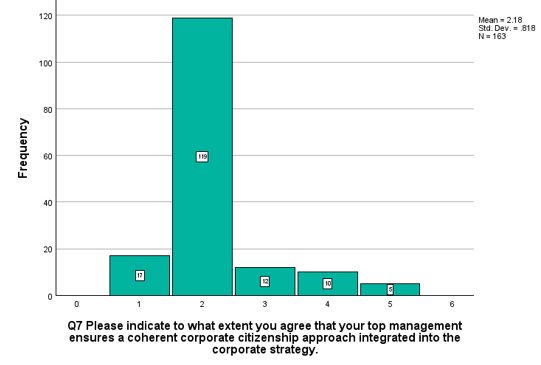

Chart 7: CSR Corporate Citizenship Approach

(Source: Author)

In response to question 7 on the integration of corporate citizenship approaches, 136 of respondents (119+17) said they agree or strongly agree that senior management guarantees a consistent approach. It seems that there is a strong desire to include CSR into the entire business plan, based on this good image (Lim and Pope, 2022). Nevertheless, it is necessary to address internal alignment in order to integrate CSR more effectively, since 10 disagree and 5 strongly disagree suggest possible differences or communication gaps among senior management (See Appendix 3).

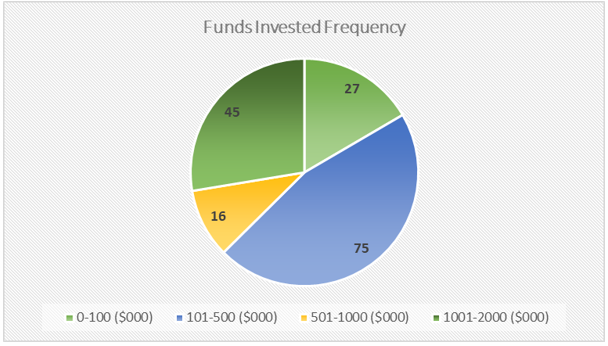

Chart 8: CSR Investment

(Source: Author)

In the previous five years, the majority respondents stated that their company (75) spent between $101,000 and $500,000 on CSR-related controls (Q8). Followed by 45 respondents who stated that their company has invested between $1,001,000 and $2,000,000 for CSR related controls. Although the distribution implies a variance in the size of expenditure, this financial commitment reflects a realisation of the value of CSR (George et al. 2020) (See Appendix 3).

2.3 Company Performance Analysis

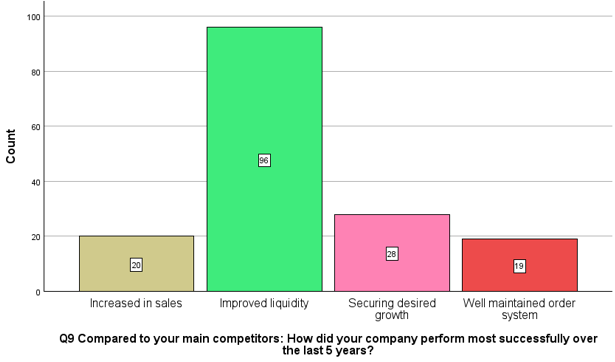

Chart 9: Company Performance

(Source: Author)

When asked to describe their performance over the last five years (Q9), 96 of respondents stated it was due to increased liquidity, while 28 stated it was due to achieving their target growth rate. This points to a success strategy that is based on money, with a focus on financial growth and stability as KPIs in the competitive environment (Zimon, 2020) (See Appendix 4).

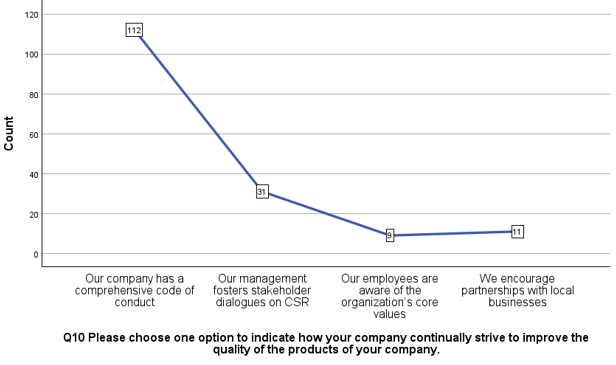

Chart 10: Product Quality

(Source: Author)

Moreover, 112 of respondents stated that having a thorough code of conduct is the technique they have selected to increase product quality (Q10). The significance of ethical norms in guaranteeing product quality is shown by the obtained responses. A larger dedication to internal and collaborative techniques for quality development is shown by 9 respondents stating employee understanding of core values and 31 emphases on stakeholder interactions (Ginting et al. 2020) (See Appendix 4).

3. Conclusion

The research sheds light on important elements that influence the management controls in SMEs that are connected to CSR. There is cause for worry over the representation of opinions due to the lack of gender balance in senior management. Moreover, the findings suggest that the results cannot be applied to smaller SMEs due to the data being heavily skewed towards large companies. Evidence of good corporate citizenship includes a desire for integrated citizenship, a willingness to financially commit to CSR controls, and a clear understanding of the importance of CSR. On the other hand, there is room for development due to the preponderance of emphasis on financial performance and the difficulties with internal alignment among senior management.

References

Almashhadani, M., 2021. Internal Control Mechanisms, CSR, and Profitability: A. International Journal of Business and Management Invention, 10(12), pp.38-43.

Bhuiyan, F., Baird, K. and Munir, R., 2022. The associations between management control systems, market orientation and CSR use. Journal of Management Control, 33(1), pp.27-79.

George, N.A., Aboobaker, N. and Edward, M., 2020. Corporate social responsibility and organizational commitment: effects of CSR attitude, organizational trust and identification. Society and Business Review, 15(3), pp.255-272.

Ginting, R., Ishak, A. and Malik, A.F., 2020, April. Product development and design with a combination of design for manufacturing or assembly and quality function deployment: A literature review. In AIP Conference Proceedings (Vol. 2217, No. 1). AIP Publishing.

Kuzior, A., Ober, J. and Karwot, J., 2021. Stakeholder expectation of corporate social responsibility practices: A case study of PWiK Rybnik, Poland. Energies, 14(11), p.3337.

Lim, A. and Pope, S., 2022. What drives companies to do good? A “universal” ordering of corporate social responsibility motivations. Corporate Social Responsibility and Environmental Management, 29(1), pp.233-255.

Maida, A. and Weber, A., 2022. Female leadership and gender gap within firms: Evidence from an Italian board reform. Ilr Review, 75(2), pp.488-515.

Sendlhofer, T., 2020. Decoupling from moral responsibility for CSR: Employees' visionary procrastination at a SME. Journal of Business Ethics, 167(2), pp.361-378.

Zimon, G., 2020. Issues of financial liquidity of small and medium-sized trading companies: A case study from Poland. Entrepreneurship and Sustainability Issues, 8(1), p.363.

Would you like to schedule a callback?

Send us a message and we will get back to you

Highlights

Earn While You Learn With Us

Confidentiality Agreement

Money Back Guarantee

Live Expert Sessions

550+ Ph.D Experts

21 Step Quality Check

100% Quality

24*7 Live Help

On Time Delivery

Plagiarism-Free

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU

81 Isla Avenue Glenroy, Mel, VIC, 3046 AU